FW

Kenya lobbying against America's trade deal with Asian states

Fearing losing its current preferential access under African Growth and Opportunity Act (Agoa), Kenya is lobbying against the planned Trans-Pacific Partnership Agreement (TPP) between US and 12 Asian states. The country joined other trade ministers from African countries at this year's Agoa forum in Washington to urge the US government to reconsider the move as it will make the goods coming from Africa uncompetitive in the market.

Trade Principal Secretary Chris Kiptoo preferences that Kenya enjoys will be eroded once the US enters into trade agreements with other states outside Africa. He maintained by saying that other trade agreements such as the Transpacific Partnership Agreement that the US is planning would affect the goods that are currently enjoying preferential rates to America.

TPP eliminates or reduces all tariffs on goods traded between partner countries. The TPP agreement would abolish many of these tariffs. Kiptoo notes that it would be difficult for Kenya to compete with countries such as Vietnam and other Asian states that are part of the TPP agreement and a big producer of the textile goods.

H&M revenue growth slows down

Swedish fast fashion brand H&M’s revenue growth slowed down by about one per cent this month, the slowest pace in more than a year. Markdowns eroded third-quarter profit margins by 1.1 percentage points. Europe’s second-largest fashion retailer plans to introduce two brands next year. The earnings outlook for next year will be helped by a gradual reduction in the pace of investment, which has been higher than normal as it prepares the new brands and adds online shopping.

H&M monthly sales have been disappointing more often than not over the past year. Pretax profit fell 9.1 per cent in the third quarter, which ran through August. Inventory surged 24 per cent, mostly due to unsold autumn wear, and that position is expected to improve. The company plans to add e-commerce in eleven markets and open 425 net new stores this financial year. In 2017 H&M intends to open stores in four to five new markets, including Colombia, Iceland and Kazakhstan.

Europe’s fashion retailers have been suffering lately from an unseasonably warm end to summer and a lack of compelling fashion trends. Business conditions are close to a recession. Price competition in the industry is escalating H&M feels the need to continue cutting prices in the fourth quarter following a weak start to the autumn season.

Lectra-ESCAP Europe hold round table on uses of customer data

Amazon, EasySize, Evo Pricing and Lectra explored diverse uses for customer data during a round table event organized by the ESCP Europe - Lectra ‘Fashion & Technology’ Chair in Paris. Lectra, the world leader in integrated technology solutions dedicated to industries using fabrics, leather, technical textiles and composite materials, the French business school ESCP Europe and their joint ‘Fashion & Technology’ Chair examined the multiple ways the fashion industry’s ecosystem can use customer data, during a recent round table event at the start of the fifth Fashion Tech Week in Paris. The speakers included: Elise Beuriot, senior category leader, EU Luggage, Amazon, Olivier Dancot, VP of data, Lectra, Fabrizio Fantini, founder and CEO, Evo Pricing, and Gulnaz Khusainova, founder and CEO, Easysize. There are multiple ways in which the fashion industry’s ecosystem can use customer data. Analysis of customer data lends itself to limitless applications along the entire fashion value chain. Its impact is immense, whether in terms of customer satisfaction, competitiveness, revenues or waste limitation.

Fashion is an industry where unsold items generate a lot of waste. Algorithms and big data analysis can reduce leftovers by anticipating demand several weeks ahead in order to optimize the price and replenishment. Fashion companies who exploit data to inform their decisions become more efficient. They are better armed to protect their margins, but can also sell for less, and potentially reach a larger number of consumers.

A wealth of data offers many sources of inspiration for stylists. For teams in charge of collections, complex models allow the analysis of data like online traffic and purchase history in order to design and offer products consumers expect, which is a priority for a company obsessed by the customer.

For editors of software dedicated to fashion, and suppliers of cutting machines designed for the clothing industry, analyzing usage data enables the offer to evolve, making each step in the value chain more efficient and perfectly adapted to the needs of brands, retailers and manufacturers.

APTMA vows to restore viability of textile industry

The Central Chairman of All Pakistan Textile Mills Association (APTMA) Aamir Fayyaz has vowed to restore the viability of the textile industry to ensure growth and sustainability. He gave the assurance while delivering his maiden speech on the occasion of the 58th Annual General Meeting of APTMA.

Fayyaz said he believed the association members rightly have a lot of expectations from APTMA as they’ve been suffering on account of major issues. He assured the members that he and his team would not leave any stone unturned for taking forward the agenda of growth and sustainability of the textile industry to an early fruition.

He stressed upon the need for harmony and unity amongst APTMA members for amicable resolution of issues. He further said he would make all out efforts to further strengthen the image of APTMA as the premier association of the textile industry in Pakistan.

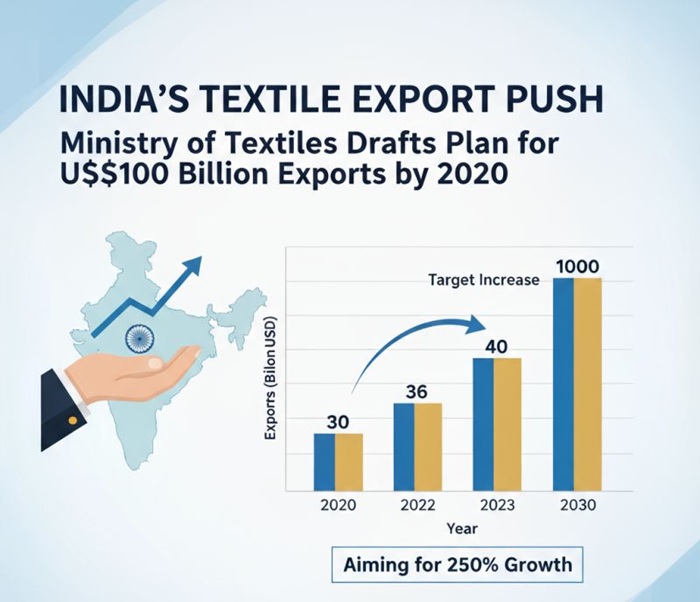

New strategies to pep up growth in India’s textile sector

"India’s textile industry has been identified as one of the thrust areas for economic growth due to its employment potential for rural masses, capability of inclusive growth, generating huge forex with least imports, etc. However, FY15-16 proved to be yet another challenging year for the textile industry especially the spinning segment due to adverse market conditions, excess production capacity, almost 50 per cent increase in cotton prices, no parity between cotton and yarn prices and the cascading effect in down-stream sectors, etc."

India’s textile industry has been identified as one of the thrust areas for economic growth due to its employment potential for rural masses, capability of inclusive growth, generating huge forex with least imports, etc. However, FY15-16 proved to be yet another challenging year for the textile industry especially the spinning segment due to adverse market conditions, excess production capacity, almost 50 per cent increase in cotton prices, no parity between cotton and yarn prices and the cascading effect in down-stream sectors, etc. As per June 2016 RBI Financial Stability Report, textile industry is amongst the top three stressed industries and in December 2015, the textile industry saw 6.4 per cent standard accounts slipping into the NPA category.

Additional funds, new policies as growth boosters

“To keep the industry thriving the Central government has taken many steps which are expected to yield long term benefits. The Centre has extended TUFS till the end of the 13th Plan and allocated Rs 12,671 crores to meet the subsidies of committed liabilities and Rs 5,151 crores to meet liabilities of ATUFS, thus totalling Rs 17,822 crores, a record allocation in the history of TUFS. Additionally, extension of 2 per cent MEIS and 3 per cent IES export benefits for all textile products except yarn. It has also enhanced duty draw back rates for various textile products,” said M Senthil Kuma, Chairman, SIMA at the 57th AGM held recently. “Meanwhile a Rs 6,000crores special package for garment exports including refund of State levies and certain land mark amendments in the labour laws like fixed term employment, optional EPF, refund of State levies, etc. was announced. The government is also directing Cotton Corporation of India to sell the balance quantity of cotton only to MSME category spinning mills that could soften cotton prices which had increased by almost 50 per cent within few months and affected the entire cotton textile value chain especially spinning sector” he explained.

Reforms with eye on future

The Confederation of Indian Textile Industry and Cotton Textile Export Promotion Council have come forward with study reports to sensitise the government about urgent measures to be taken to increase exports. To cope with the serious crisis rising in the cotton front as the associations have also urged the government to bring back Technology Mission on Cotton in a revised format and increase yield. Kumar said “As cotton prices are becoming highly volatile , mills are not being able to compete with traders and multinational companies, who cover cotton during season, export sizable volume, create scarcity and increase prices. As a major advantage the power cost in general has come down drastically and it is likely to decrease further in the coming years due to abundant availability of power in open access thus making the industry globally competitive. The government has also brought notable changes during the year on fixed term employment, optional PF, employer’s EPF contribution by the government, etc. At the same time, certain labour policies have been devised to increase the cost of production for the manufacturing sector include increase in minimum wages, ESI ceiling, bonus ceiling. With various schemes to support the industry, the country is expected to see large scale employment and significantly increase its contribution to the country’s overall GDP and forex,” he said.

On textile policies he said though a number of states had announced industrial policies containing a slew of measures to attract investments in the textile sector, we are yet to get announcement of Tamil Nadu Textile Policy and the National Textile Policy. “With the new Textile Minister at the helm, we look forward to the announcement of the Policy at an early date and we hope the State Policy would follow soon” he explained. He summed up by saying, “With various schemes supporting the industry in place, I am confident that the industry would leap ahead by creating large scale employment and increase its contribution to the country’s GDP and Forex earnings significantly.”

Report shows Sri Lanka’s apparel exports caters more to niche markets

Rather than concentrating on volume products, Sri Lanka’s exports are designated to more towards niche and fashion-oriented markets, reveals a new report. The Business Information Division of the Ceylon Chamber of Commerce has released its latest review conducted on the apparel industry. As per the report, the country’s export products differs from other South Asian countries as Sri Lanka excels in producing intimate apparel, sportswear, trousers and swimwear. The report says the exports have been equally divided between cotton and man-made fiber products.

The latest publication also gives information on an overview of the world apparel industry, market share of neighbouring countries in South Asia. It also contains Sri Lanka’s apparel sector in brief, apparel sector exports during the last five years, top importing and exporting countries of apparels, HS Code wise exports statistical analysis and views of industry experts of the trade.

Première Vision proves ideal platform for eco fashion hub

This month's Première Vision exhibition proved to be the ideal platform for eco-fashion hub, C.L.A.S.S (Creativity, Lifestyle And Sustainable Synergy), whose presentation included several eco smart innovation stories that were of major interest to buyers from the knitwear sector. Attracting a great deal of attention was the A Stelloni collection by Mapel.

Here, Re.Verso was the identifying trademark of a new, totally traceable, certified and transparent, Italian textile system concerning wool materials. The supply chain is based on wool and cashmere pre consumer clippings, supplied by the best Italian and international brands and producers of the fashion industry. This innovative and exclusive system allows great savings in terms of energy, water consumption, and CO2 emissions, as certified by the LCA (Life Cycle Assessment) done by Prima Q.

Five premium textile Italian makers viz Green Line and Nuova Fratelli Boretti for the raw material, A Stelloni Collection By Mapel for fashion textiles, Filpucci for high-end, luxury knitwear yarns and Filatura C4 for contract and woven yarns were involved. Products on the show included Re.Verso Baby Camel, a soft and delicate yarn, with a unique touch that preserves all the natural, luxury proprieties of Baby Camel and reveals the unique and precious nuances tuned with most contemporary, deluxe aspirations that will be added to the Smart DNA of Re.Verso. Brands that have adopted this collection include Eileen Fisher, Stella McCartney, Filippa K and Patagonia, and Front Runners.

Polyester staple fiber market to grow at 7.5 per cent

The global polyester staple fiber market is expected to grow at a CAGR of 7.5 per cent from 2016 to 2024. In terms of volume, the polyester staple fiber market is expected to expand at a CAGR of four per cent between 2016 and 2024.

Polyester staple fiber has emerged as the fastest growing fiber amongst all types of fibers. Polyester staple fibers are used in a wide range of applications such as carpets and rugs, fiberfill and nonwoven fabrics, home furnishings, and apparels. They are being used in mattresses and pillows. Demand for specialty mattresses is rising due to the high consumer preference for eco-friendly and health-promoting products.

In the global cotton-dominated apparel market, polyester staple fiber has emerged as the fastest-growing segment in the recent past. The major reasons behind its increasing demand are its inherent good quality and the premium fetched by blended yarns in international markets. Solid polyester staple fiber is considered the leading polyester staple fiber with a total global share of more than 65 per cent in 2015.

Apparel was the largest end-use segment of the global polyester staple fiber market in 2015. It was followed by home furnishing and personal care and hygiene.

Pakistan’s cotton exports fall

Pakistan’s export of cotton products have decreased during the last three years. The reasons include inconsistency in yield of cotton crop, rising cost of business, shrinking global demand and decrease in cotton prices in the market. The country exported cotton products worth $11 billion during 2015-16. These comprise raw cotton, cotton yarn, cotton cloth, cotton carded or combed, knitwear, bed wear, towels, tents, canvas and tarpaulin and readymade garments.

Steps have been taken to enhance exports of cotton products. Electricity tariff has been reduced for industrial units in order to reduce the cost of doing business. The export sector is getting easy finance. Discount rate, which currently stands at six per cent has been reduced. The export finance rate currently at 3.5 per cent is the lowest in a decade especially for the textile sector.

Under the textile policy 2015-19, an amount of Rs 64.15 billion would be spent on the textile sector to double the exports of textiles and clothing from the existing 13 billion dollars to 26 billion dollars by the year 2019. Pakistan is the fourth largest producer of cotton in the world and holds the third largest spinning capacity in Asia after China and India.

Ongoing Filo Milan trade fair has exhibitors galore

This week leading experts in the textile industry are exhibiting their latest products and innovations at the 46th edition of the Filo Milan trade fair for yarns and fabrics which is taking place at the Palazzo delle Stelline. The venue has Monocel, a designer and distributor of high-end top dyed yarns under the Monocel brand demonstrating its potential and how it can represent the next generation of smart cellulosic yarns. The company is exhibiting its Monocel yarns in a range of jersey and woven fabric innovations.

Monocel is a new generation of smart and responsible lyocell-from-bamboo yarns. These developments represent a new option in eco-responsible yarns, with a unique colour range delivered through an Ultrasonic Natural Plant Dyed process, the company reports.

Monocel Ultrasonic Plant Dyed yarns is a family of high tech top dyed yarns. It combine the latest advanced dyeing technology with ancient coloration materials. The company says it believes it is one of the most advanced water saving techniques available. The patented process uses liquid plant dyes in the new ultrasonic ‘attachment’ technique for a high level of colour fastness, with encouraging improved efficiencies in energy and emissions reductions through lower temperatures and shorter dyeing times.

By combining Monocel with natural plant dyes, the company has achieved a beautiful colour range that is unique to the ultrasonic process and offers yarns that are completely non-toxic and gentle to the skin. The dyes are based on traditional Asian medicinal roots, fruits and flowers.

Yarns come in pure Monocel or blended with GOTS certified organic cotton, spun in Siro-Compact, and Compact formats for the finest yarns. White bleached yarns use the more environmental Hydrogen Peroxide (H2O2) process.

Marchi & Fildi, a leading spinner and provider of cotton based yarns for the textile industry, is presenting its Ecotec yarn, made in Italy and produced by an exclusive traceable and certified production process that transforms pre-dyed textile clippings into a 100% cotton yarn with record savings in water and energy consumption, according to the manufacturer.

According to the company, Ecotec is the new generation of smart cotton. Thanks to the exclusive Marchi & Fildi process, the redundant remnants from the fashion system’s garment production are recovered and transformed into Ecotec yarns, amking it possible to use less resources while maintaining the quality standards.

Some companies decided to become Ecotec accredited partners by signing the Ecotec policy that makes them active part of the Ecotec marketing and communication activities. These include Euromaglia S.r.l, Lana Reale, Manifattura CBM, Tessuti & Tessuti srl, Tintex Texteis Sa, Karalis Sa.

Ecotec is a refined and versatile yarn that is suitable for woven and jersey fashion fabrics as well as for knitwear and hosiery. This year Ecotec by Marchi & Fildi is presenting two product lines at the Fair including Ecotec Innovation, a line of smart solutions created by the R&D department of Marchi & Fildi, in cooperation with a textile style office; and Ecotec Collection, an exclusive range of Ecotec fabrics made by accredited Ecotec partners.