FW

Bangladesh RMG transitions to a strategic stabilization phase

The Bangladesh ready-made garment (RMG) sector is transitioning from a period of severe operational volatility toward a strategic stabilization phase. Fiscal Year 2024-25 concluded with apparel exports reaching $39.34 billion, a resilient 8.84 per cent growth despite a sequence of unprecedented disruptions. The industry weathered a ‘perfect storm’ in 2025, including a devastating airport cargo fire that caused an estimated $1 billion in losses, political transitions, and a 9 per cent statutory wage hike. While export momentum slowed to a 2.53 per cent increase in the January–November 2025 window, a decisive diplomatic breakthrough - capping US ‘reciprocal’ tariffs at 20 per cent instead of the feared 35 per cent - has significantly revived buyer confidence and order flows for the upcoming spring/summer 2026 season.

Modernization and high-value diversification

To counter rising overheads and the withdrawal of traditional export incentives, manufacturers are accelerating a move into high-margin segments. This shift is evident in the 9.73 per cent growth of knitwear exports ($21.15 billion) compared to the 7.82 per cent rise in woven garments. Leading players are diversifying into Man-Made Fibers (MMF) and functional outerwear to bridge the gap as Bangladesh prepares for its 2026 LDC graduation. The 2025 shocks acted as a catalyst for efficiency; we are no longer just a volume hub but a partner in complex, technical fashion, notes Senior Director, BGMEA.

Sustainability as a shield against global headwinds

Environmental, Social, and Governance (ESG) compliance has become the sector’s primary defense against intensifying competition from Vietnam and India. Bangladesh now leads the world with over 240 LEED-certified green factories, a status that attracted significant order diversions in late 2025 as European retailers tightened circularity requirements. Despite the closure of approximately 113 underperforming units over the last 15 months, the establishment of 128 sophisticated, automated factories signals a structural consolidation. Industry experts project a robust recovery starting in the second quarter of 2026, supported by eased inflationary pressures and a more stable domestic energy grid.

Bangladesh is the world's second-largest apparel exporter, with the RMG sector contributing 81 per cent of national export earnings. Dominating in knitwear and woven categories, the industry targets a $100 billion export goal by 2030. Originally built on low-cost basics, it is now a global leader in green manufacturing and sustainable fashion.

The Circular Yield Why 2026 is the year sustainability paid the dividend

As the global textile industry moves through the final quarter of the year, this feature serves as a cornerstone of our "Wrap Up 2025, Outlook 2026" series, charting the transition from experimental sustainability to scaled industrial reality. While 2025 was defined by the pressure to decarbonize, 2026 is emerging as the year where circularity finally aligns with capital efficiency.

The Bio-Fabrication Leap: Can mushrooms compete with cotton?

For years, bio-fabricated fibers like mycelium (mushroom root) and algae were the darlings of experimental luxury—cool, avant-garde, and prohibitively expensive. However, 2026 marks the "Industrial Leap" where these materials hit the mainstream shelf. The bio-based textile market, valued at $54.21 billion in 2025, is projected to surge toward $113.43 billion by 2034, with a significant acceleration beginning this year.In 2026, the sector is witnessing a decisive transition: Bio-Industrialization. The narrative has moved from proving the science to perfecting the supply chain.

The most compelling metric for the C-Suite in 2026 is the closing price gap. For the first time, the "Green Premium" is eroding. While conventional cotton remains volatile—hovering around $0.70 to $0.85 per pound—bio-synthetic alternatives like PHA (polyhydroxyalkanoates) and microbial cellulose are achieving price parity in high-performance segments. By 2026, the cost to produce bio-fabricated leather alternatives has dropped by nearly 30% compared to 2023 levels, thanks to decentralized "fermentation hubs" that utilize agricultural waste as feedstock.

"Scalability is no longer a chemistry problem; it’s a capacity problem," notes a leading Material Science Officer at a Tier-1 mill. "In 2026, we aren't just buying a story; we’re buying consistent, high-tenacity fiber at a predictable volume."

The ‘Mono-Material’ Transition:Designing for the end

The most significant technical development for 2026 is occurring at the yarn level: the Mono-Material Revolution. Throughout 2025, the industry leaned heavily on "recycled blends"—typically a mix of recycled polyester and organic cotton. While these served a marketing purpose, they created an end-of-life bottleneck. These blended fibers are notoriously difficult to separate, making them a one-way ticket to a secondary landfill.

In 2026, the strategic focus is toward Polyester-based Mono-Stretch Yarns, valued at $1.04 billion in 2026, this segment is projected to grow at a 9.5% CAGR.

By replacing traditional spandex—a contaminant in the circular loop—with specialized elasto-polyesters, manufacturers are creating garments that can be recycled as a single unit without mechanical stripping. Analysts project that these mono-materials will capture nearly 38% of the performance yarn market by the end of 2026.This transition allows a garment to be shredded and pelletized back into virgin-quality yarn without the chemical nightmare of separating elastane from cotton. For the CFO, this isn't just an environmental win—it’s an insurance policy against the EU’s looming ban on the destruction of unsold goods, effective July 19, 2026, for large enterprises.

|

Material Segment |

2025 Market Share |

2026 Projected Share |

Growth Driver |

|

Traditional Blends (Poly/Cotton) |

58% |

42% |

Recycling Complexity |

|

Mono-Material Synthetic Stretch |

22% |

38% |

Circular Mandates |

|

Cellulosic Bio-Based Fibers |

9% |

14% |

Scaled Production |

Advanced Recycling: Closing the loop on post-consumer waste

While mechanical recycling has been the industry standard, 2026 marks the year Chemical Recycling achieves commercial viability. Unlike mechanical methods, which shorten fiber length and degrade quality, chemical depolymerization breaks fibers down to the molecular level, allowing them to be rebuilt into "virgin-quality" yarns.

The financial logic is compelling. While chemical recycling remains more capital-intensive than mechanical shredding, the output commands a "Virgin-Grade" premium. As one CFO recently stated during a 2026 strategy session, "Investing in chemical recovery isn't a cost; it’s our future feedstock security in a world where virgin resource prices are becoming increasingly volatile.

Monetizing the Redo: Reverse logistics as a profit center

If 2025 was the year of exploring resale, 2026 is the year of Integrated Reverse Commerce. For the first time, C-Suite leadership is viewing resale and repair not as PR stunts, but as critical margin-preservation strategies. The global resale market is projected to reach $338.4 billion by 2026, growing three times faster than the broader retail sector.

Brands are no longer handing off their secondhand business to third-party marketplaces. Instead, they are becoming their own secondhand competitors. By owning the "Take-Back" infrastructure, brands capture the data and the profit from the second, third, and fourth life of a garment.

Trade Barriers and Green Protectionism: The new global map

The 2026 trade landscape is being redefined by "Green Protectionism." Free Trade Agreements (FTAs) are no longer just about lowering tariffs; they are becoming instruments of environmental policy. Under the EU’s Carbon Border Adjustment Mechanism (CBAM), which enters a critical phase in 2026, importers will begin facing actual costs associated with the carbon footprint of their textile imports.

Various countries are adapting through "Green Corridors." India and Vietnam, for example, are leveraging their FTAs to incentivize circularity by offering "Fast-Track" customs clearance for products that utilize verifiable recycled or bio-based content. Conversely, "Linear" products—those with high carbon footprints and zero recyclability—are facing what many call "Carbon Surcharges," effectively a secondary tariff that erodes any cost advantage gained from low-cost labor.

|

Region |

Primary Trade Shift 2026 |

Key Indicator |

|

European Union |

Digital Passport Enforcement |

95% compliance required for entry |

|

United States |

Forced Labor & Transparency Audits |

Shift toward nearshoring (Mexico/CAFTA) |

|

India |

Scale-up of PM MITRA "Green Parks" |

11.4% growth in "circular-ready" clusters |

|

Vietnam |

Transition to Renewable Energy Mills |

25% reduction in mill carbon intensity |

C-Suite Strategic Leadership: The "Finance-Grade" ESG era

The final piece of the 2026 puzzle is the death of vague marketing. In 2025, marketing teams could lead with "eco-friendly" slogans. In 2026, Sustainability is a Financial Audit. Banks and institutional investors have tightened the screws; capital access is now directly linked to verifiable, "Finance-Grade" ESG data.

C-Suite leaders are now hiring sustainability accountants to map the "Residual Value" of inventory on the balance sheet. A warehouse full of 100,000 mono-material, recyclable jackets is now viewed as an asset of recoverable raw material, whereas a warehouse of non-recyclable blends is increasingly seen as a future disposal liability. This transparency gold rush is fueling a new tech ecosystem where blockchain-backed supply chain data is the price of admission for global trade.

Editor Concludes: The year the dividend arrived

The outlook for 2026 is one of pragmatic optimism. We are leaving behind the era of "doing less harm" and entering the era of "doing more business" through circularity. The companies that will dominate the 2026 landscape are those that have successfully transitioned from a volume-based mindset to a value-retention mindset.

As the CFO’s playbook changes to account for the secondary and tertiary value of every fiber, the divide between the "Circular Leaders" and the "Linear Laggards" will become an unbridgeable chasm. The circular yield is no longer a distant promise; it is the new bottom line.

Indian textile engineering industry pivots to digital-first manufacturing ecosystem

The Indian textile engineering landscape is undergoing a fundamental transformation, shifting from legacy mechanical processes to a digital-first manufacturing ecosystem. At the third edition of the India ITME Technical Awards 2025 in Mumbai, industry leaders signaled that the sector has reached a critical inflection point where high-tech adoption is no longer optional. With the domestic textile market projected to reach $190 billion by 2025–26, the integration of Artificial Intelligence (AI) and the Internet of Things (IoT) has emerged as the ‘third partner’ in production. This shift is designed to address systemic challenges such as labor-intensive quality control and energy inefficiencies, enabling Indian manufacturers to compete more aggressively in a global market that is increasingly demanding precision and speed.

Bridging heritage with advanced design

A significant news angle emerging from the summit is the strategic rebranding of traditional industries, specifically Khadi, as high-performance growth engines rather than philanthropic ventures. Roop Rashi Mahapatra, CEO, Khadi & Village Industries Commission (KVIC), emphasized, the future of traditional textiles lies in a ‘design-led’ approach that leverages modern engineering to create sustainable livelihoods. By combining ancient craftsmanship with contemporary machinery, the industry aims to create a circular economy where eco-friendly fibers like hemp and banana - standardized by 2025 - can meet the rigorous technical standards of international export markets. This convergence of heritage and technology is seen as a primary driver for the 10 per cent Y-o-Y export growth recorded in late 2025.

Recognizing the champions of sustainable engineering

The 2025 awards underscored a move toward "principled consumption" and localized innovation. Yamuna Machine Works was recognized as a champion in Processing and Finishing, while Zydex Industries took top honors for sustainability-centric initiatives. Notably, the industry is seeing a ‘startup mindset’ among young engineers who are developing cutting-edge solutions for fabric defect detection and thermal regulation. These innovations are critical as the sector faces rising raw material costs and shifting cotton sourcing patterns. The ‘Make in India’ vision was further solidified by Rieter India’s award for successful technology transfer, highlighting the country's growing capacity to manufacture world-class textile machinery domestically.

The India International Textile Machinery Exhibitions (ITME) Society is the apex non-profit industry body dedicated to promoting textile engineering and technology in India. Established in 1980, it serves as a global platform for technology transfer and trade. The Society currently focuses on the ‘Vision 2047’ roadmap, aiming to establish India as a global textile machinery hub. With the sector contributing 2.3 per cent to national GDP, the Society’s initiatives support a workforce of over 45 million by fostering academic-industry partnerships and accelerating the adoption of Industry 4.0 standards across the textile value chain.

Depop’s ‘Edited Self’ strategy triggers 54% US growth

In a strategic departure from the ‘fast-fashion’ frenzy, resale giant Depop is capitalizing on a fundamental shift in Gen Z behavior: the transition from algorithmic churn to personal authorship. According to Depop’s 2026 Trends Report, ‘The Edited Self,’ consumers are actively rejecting micro-trends in favor of ‘repeatable staples.’ This intentionality is not merely a stylistic pivot but a high-velocity business driver. Amidst a broader US retail landscape characterized by low single-digit growth and tariff-induced price hikes, Depop’s US market grew by 54 per cent in 2025. By prioritizing ‘Modern Uniforms’—sharp tailoring and dependable workwear—over disposable aesthetics, the platform has successfully positioned itself as a hedge against economic volatility.

Data-Driven Resilience and AI Integration

The fiscal impact of this ‘purposeful style’ is substantial. Depop’s Gross Merchandise Sales (GMS) hit $249.6 million in Q2, FY25, a 35.3 per cent Y-o-Y increase. To sustain this momentum, the platform is integrating "agentic commerce," using AI-powered tools that transform a single product photo into a professional listing. ‘We are seeing a cultural recalibration where taste is the new currency,’ says Peter Semple, CEO, Depop. This technological edge addresses the primary challenge of the resale sector: scalability. As 75 per cent of US shoppers now trade down to secondhand alternatives to offset inflation, Depop’s ability to offer "archival" reliability at a fraction of the cost of new apparel is reshaping the competitive hierarchy of the $82 billion resale market.

Recommerce as a strategic retail pillar

Beyond the digital storefront, Depop’s expansion into physical "pop-ups" in New York and other urban hubs reflects a move toward a ‘phygital’ retail network. This strategy leverages the ‘treasure hunt’ experience that 60 per cent of global consumers now seek when shopping secondhand. The environmental narrative remains a potent conversion tool; with 3 out of 5 Depop purchases displacing the need for brand-new items, the platform is converting "eco-anxiety" into brand loyalty. As traditional retailers struggle with overproduction, Depop’s model—fueled by a community of 43.5 million users - proves that in 2026, the most newsworthy growth is found not in the new, but in the newly rediscovered.

Depop is a global community-powered marketplace specializing in affordable, circular fashion for Gen Z and Millennials. Operating primarily in the UK and US, the Etsy-owned platform hit a peak GMS of nearly $800 million recently. Its 2026 strategy focuses on ‘Where Taste Recognizes Taste,’ scaling through AI-enabled listings and physical New York-centric retail experiences to dominate the booming global recommerce sector.

Agile US brands double down on retail expansion in 2026

While much of the US retail landscape remains cautious amid shifting trade policies and low single-digit growth projections, a elite group of ‘agile’ brands is doubling down on expansion for 2026.

Leading this charge is Uniqlo, which is slated to open 11 new stores - including its first flagship locations outside New York City in Chicago and San Francisco. This growth is underpinned by a ‘true private-label model’ where the Japanese giant controls everything from fabric production to final sale. Industry analysts suggest this full vertical integration allows Uniqlo to offer high-quality ‘LifeWear’ at prices that traditional middle-market retailers, burdened by fragmented supply chains and a 25 per cent hike in grocery-driven inflation, simply cannot match.

Off-price resilience in a cautious climate

Parallel to the vertical giants, the off-price sector is emerging as a primary growth engine for 2026. Nordstrom Rack is executing a massive sprint, with over 21 new locations announced for the upcoming year. This ‘laser focus’ follows the Nordstrom family’s $6.25 billion move to take the company private, a transition designed to shield long-term retail strategies from short-term public market pressures. By positioning stores within 15 minutes of key suburban hubs, off-price leaders are capturing ‘cash-strapped but quality-conscious’ shoppers who are increasingly trading down from department stores but refusing to sacrifice brand-name reliability.

AI and the personalization paradox

The 2026 retail roadmap is not just about physical square footage; it is a battle for data-driven precision. While 75 per cent of consumers are reportedly trading down to cheaper alternatives, they simultaneously demand premium experiences, such as two-hour delivery and AI-guided styling. Retailers are responding by integrating Generative AI for ‘agentic commerce,’ where algorithms don't just recommend products but proactively manage inventory and hyper-personalize the shopping journey. This tech-enabled efficiency is expected to be the ‘structural pillar’ that separates the 2026 market leaders from legacy players struggling with margin erosion.

Uniqlo USA: The global LifeWear standard

Uniqlo is the flagship brand of Fast Retailing, offering functional, high-quality ‘LifeWear’ across 78 US stores. Celebrating its 20th year in America, the brand targets 200 North American locations by 2027. With $2.9 billion in recent international revenue, Uniqlo leverages RFID tech and a 100 per cent private-label model to dominate the global casual-wear market.

Vietnam textile sector pivots to ‘Green & Smart’ to secure $50 billion target by 2026

As Vietnam cements its role as the world’s third-largest apparel exporter, the industry is undergoing a radical shift from labor-intensive processing to high-tech automation. By 2026, the sector is targeting a breakthrough export turnover of $50 billion, driven by a dual-transformation strategy: ‘greening’ and ‘digitalization.’ Leading manufacturers like Vinatex and TNG are increasingly deploying AI-powered vision systems for fabric defect detection and robotic packaging units, which can replace up to six workers per station. This technological leap is critical as the industry faces a 7.2 per cent mandatory wage hike and a tightening labor market.

Sustainability becomes the new export passport

The 2026 outlook is dominated by the EU’s Digital Product Passport (DPP) and Carbon Border Adjustment Mechanism (CBAM). Compliance is no longer optional; it is the ‘entry ticket’ to the European market. Vietnamese firms are responding by adopting Cold-Pad-Batch (CPB) dyeing technology, which slashes water and electricity use by nearly 73 per cent. ‘Our strategy is moving beyond low costs toward 'principled production' that satisfies the traceability demands of global giants like Nike and Adidas,’ states a representative from VITAS

Market diversification amid global headwinds

To mitigate risks from US tariff fluctuations, Vietnam has successfully diversified its footprint across 138 markets, with emerging hubs in the Middle East and Africa showing double-digit growth. Vinatex, specifically is targeting a $760 million revenue in 2026 by focusing on high-value technical apparel for the healthcare and aviation sectors. While the global demand growth rate may cool to 3 per cent, Vietnam’s move toward Original Design Manufacturing (ODM) and a 60 per cent localization rate is expected to keep margins resilient.

Vinatex: Vietnam’s national textile powerhouse

As a state-controlled giant, Vinatex leads the nation’s ‘green and digital’ roadmap across yarn, dyeing, and garment sectors. Dominating the US and EU markets, the group is aggressively localizing raw materials to reduce import reliance. Historically the industry backbone, Vinatex targets a record $57 million profit by 2026.

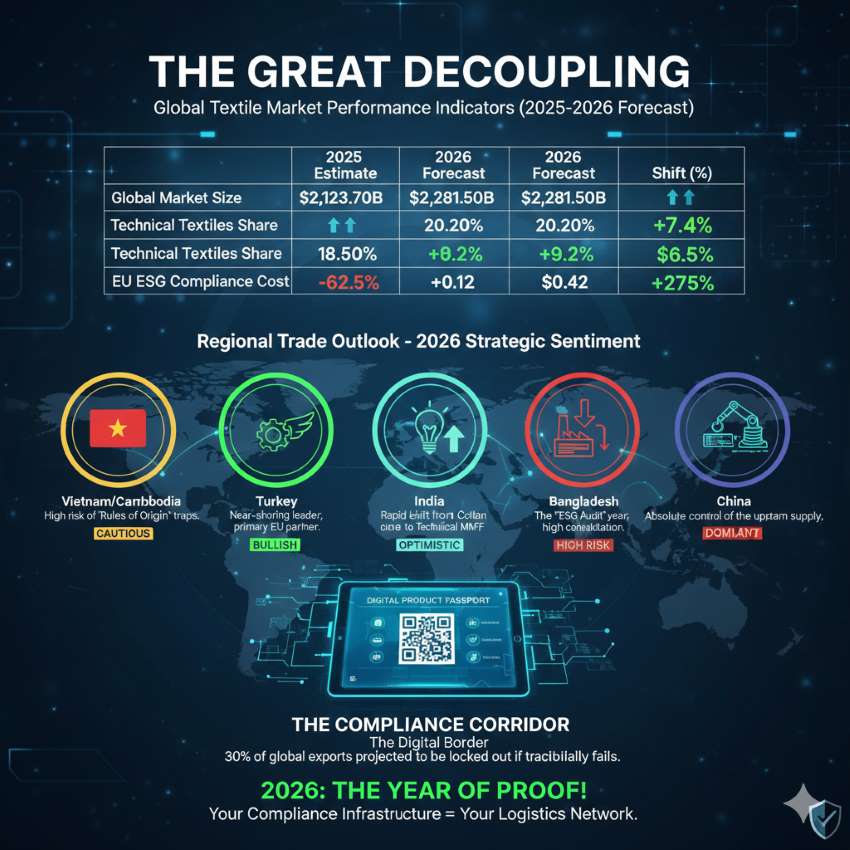

The Great Decoupling: The global play and regional and country trade outlook

This feature marks the second article in our exclusive series, "Wrap Up 2025 | Outlook 2026," where we dissect the structural shifts redefining the B2B textile and apparel landscape.

As the final bobbins of 2025 spin to a halt, the global textile and apparel industry is not merely turning a page; it is burning the old playbook. While 2025 was defined by a desperate race to dodge the "Reciprocity Tariffs" of a volatile US trade regime, 2026 is emerging as the year of the Compliance Corridor—a structural reality where market access is no longer dictated by the lowest bid, but by the most robust data set. The overarching play and role of countries in this new era is dictated by a historic structural bifurcation. For the global sourcing community, the focus has shifted from simple labor arbitrage to navigating a "Digital Border" where a product's entry into the European Union or North America depends on a verifiable "Data Birth Certificate."

The Regional Trade Outlook for 2026 confirms that we are moving toward a period of profound structural permanence. By mid-2026, the EU’s Digital Product Passport (DPP) registry and the Corporate Sustainability Due Diligence Directive (CSDDD) will go live, effectively creating a regulatory wall projected to lock out nearly 30% of current global exports that fail the traceability test.

The Global Macro View: A two-speed trade reality

Trade dynamics in late 2025 were characterized by "Pre-emptive Shipping." Importers in the United States front-loaded inventories to hedge against tariff spikes, while European buyers braced for the implementation of the EU Strategy for Sustainable and Circular Textiles. This has created a "Bullwhip Effect" heading into 2026: a cooling of demand as brands digest excess stock, followed by a frantic search for "Safe Havens"—territories with stable Free Trade Agreements (FTAs) and low geopolitical friction.

While the global textile market is projected to reach $2.28 trillion in 2026, the growth is no longer uniform. Technical textiles and Man-Made Fibers (MMF) are growing at double the rate of traditional apparel, reflecting a C-suite obsession with high-performance applications in the automotive, medical, and defense sectors.

Table 1: Global Textile Market Performance Indicators (2025–2026 Forecast)

|

Metric |

2025 Estimate |

2026 Forecast |

Shift (%) |

|

Global Market Size (USD Billion) |

$2,123.70 |

$2,281.50 |

+7.4% |

|

Technical Textiles Share (%) |

18.50% |

20.20% |

+9.2% |

|

US Sourcing Costs (Avg. YoY) |

+12.0% |

+4.5% |

-62.5%* |

|

EU ESG Compliance Cost per Unit |

$0.12 |

$0.45 |

+275% |

*Reflects stabilization after the 2025 tariff shock.

Vietnam and Cambodia: The middlemen’s dilemma

Vietnam and Cambodia enter 2026 as the primary beneficiaries of the "China-Plus-One" strategy, yet they are walking a regulatory tightrope. Despite a projected $46 billion in exports for Vietnam in 2025, a "Transparency Gap" remains. OECD (Organisation for Economic Co-operation and Development) data reveals that 20–30% of the value-added in their exports—specifically high-performance fabrics—still originates in China. As "Rules of Origin" enforcement becomes automated through AI-driven customs tracking, these nations face a "Compliance Cliff." To maintain their 2026 trajectory, they are being forced to localize their upstream supply chains, moving away from simple assembly toward domestic spinning and weaving to satisfy both USMCA (United States–Mexico–Canada Agreement)-style "Yarn Forward" rules and EU traceability mandates.

Turkey & North Africa: The speed king’s dominance

Turkey has secured its position as the definitive "Speed King" for the European market, delivering "Green Denim" within a 14-day window. Strategic proximity allows Turkish and Moroccan exporters to reach European capitals by road in under 72 hours, bypassing the volatility of 2026 ocean carrier surcharges. This is a massive commercial lever; near-shoring to Turkey now provides an estimated 12% landed-cost saving over traditional Asian routes when accounting for transit-tied capital and new regulatory premiums. By 2026, Turkey is no longer just a sewing hub but the "Technology Hub for Global Denim," leading the transition to waterless dyeing and circular material usage.

India: Scaling the technical upgraders

India is executing a massive industrial upgrade, moving "Beyond Basic Cotton." Leveraged by the government’s Production Linked Incentive (PLI) scheme, Indian industrial giants are scaling up in high-value MMF and Technical Textiles. India’s technical segment is expected to hit a 10% CAGR by the end of 2026, offsetting headwinds in traditional cotton knits. As one industry leader stated, "We are no longer just the world’s cotton patch; we are becoming a high-complexity material partner." This diversification into automotive and medical textiles has allowed India to remain resilient despite fluctuating global demand for fast fashion.

Bangladesh: The €18 bn question of compliance

For Bangladesh, 2026 is the year of "Compliance or Collapse." Following its scheduled graduation from Least Developed Country (LDC) status in November 2026, the nation faces the potential loss of the EU's "Everything But Arms" (EBA) preferences. While the EU has offered a transition period until 2029, the immediate pressure lies in the mandatory labor and environmental audits under the CSDDD. 2026 is becoming a period of intense consolidation; global brands are narrowing their supplier bases to only those who can provide real-time visibility into wage transparency and chemical discharge. Bangladesh must decide whether to invest billions in green infrastructure or risk losing its most lucrative trade partner.

China: The upstream giant and global supplier

China has successfully transitioned to become the "Supplier to the World's Suppliers." While its share of finished apparel assembly has slipped, its grip on global textiles; yarns, fabrics, and chemicals has grown to a commanding 43%. In 2026, China effectively owns the "guts" of the global industry. Even as a garment is sewn in Southeast Asia, the technology and material that made it likely originated in a smart-mill in Zhejiang. China’s 2026 strategy is one of "Industrial Supremacy through Innovation," focusing on chemically recycled fibers and high-automation that competitors cannot yet match at scale.

Table 2: Regional Trade Outlook - 2026 Strategic Sentiment

|

Region |

Status |

The 2026 Narrative |

Market Sentiment |

|

Vietnam |

The Middleman |

High risk of "Rules of Origin" traps. |

Cautious |

|

Turkey |

The Speed King |

Near-shoring leader; primary EU partner. |

Bullish |

|

India |

Scale Upgrader |

Rapid shift from Cotton to Technical MMF. |

Optimistic |

|

Bangladesh |

Compliance Gamble |

The "ESG Audit" year; high consolidation. |

High Risk |

|

China |

Textile Giant |

Absolute control of the upstream supply. |

Dominant |

C-Suite Strategic Outlook: The "Asset-Light" CEO

The leadership model for 2026 is the Asset-Light CEO. Strategic leaders are moving away from owning the entire production line toward a "Supply Web" model, utilizing Manufacturing-as-a-Service platforms to launch collections without heavy inventory. CFOs are now treating "Reverse Logistics" not as an expense, but as a secondary revenue stream. Resale, repair, and rental models are being integrated directly into balance sheets as brands seek to meet the EU's new longevity standards. Leadership in this era is about managing data as much as fabric; if you cannot prove your product's journey from Tier-4 raw material to the retail floor, you simply do not have a product in 2026.

Editor’s Conclusion: The dawn of total transparency

As we look toward the 2026 horizon, the "Great Decoupling" of the textile industry is final. We have decoupled from the belief that cheap labor is a permanent competitive advantage and from the "Black Box" supply chain where the origin of raw materials was a mystery. The winner of 2026 is the Transparent Brand-the one that can provide a "Data Birth Certificate" for every garment. Trade policies and FTAs are no longer just about taxes; they are about values and verifiable proof. In this new era, your compliance infrastructure is just as vital as your logistics network. 2026 is the year of Proof!

Suit Direct flagship lands in Liverpool: A high-stakes bet on occasion wear

Menswear brand Suit Direct has officially inaugurated its new flagship store on Liverpool’s Paradise Street, marking a critical milestone in its nationwide retail expansion. Inaugurated on December 19, 2025, the store opens as currently valued at approximately £16.2 billion - the UK menswear market witnesses a significant shift toward service-led, physical retail experiences. Despite a broader cooling of consumer spending, the occasion wear segment remains a resilient outlier, with Suit Direct targeting high-growth categories like weddings, proms, and premium racing events.

Elevating the ‘Phygital’ tailoring experience

The Liverpool site serves as a blueprint for the brand’s ‘elevated’ retail concept, prioritizing personalized 1-to-1 styling and bookable appointments to combat the surge in online-only competition. ‘This city loves to dress well,’ noted Amanda Argent, Retail Director,Baird Group, during the launch. The store design integrates strategic ‘pause points’ and visual storytelling to increase dwell time, a metric that has become the new gold standard for high-street success. This physical investment is backed by a robust digital strategy; recent data shows, while online conversion rates for suit retailers can be volatile, Suit Direct has managed to maintain industry-leading efficiency with a 32 per cent increase in ROI through enhanced sizing guides and localized stock visibility.

Strategic diversification into ‘Modern Lifestyle’

While formalwear remains the brand's core, the new flagship highlights a significant expansion into lifestyle and smart-casual ranges, including knitwear and chinos designed for ‘work-to-weekend’ versatility. This move aligns with a 2025 industry trend toward ‘Mix-and-Match’ tailoring, where traditional blazers are increasingly paired with denim or premium knitwear. To sustain this momentum, parent company Baird Group has confirmed plans to open up to 50 new locations across the UK by 2026, leveraging its vertical integration to offer premium labels like Ted Baker and Marc Darcy at competitive price points.

A premier UK menswear specialist with a heritage dating back to 1894, the Leeds-headquartered Baird Group operates as a vertically integrated entity under Arafa Holding, managing everything from fabric production to retail through its primary fascia, Suit Direct. The group specializes in formalwear and modern lifestyle apparel, catering to the UK and European markets with a portfolio of iconic brands including Ted Baker (under master license), Ben Sherman, and Racing Green. With a focus on aggressive high-street expansion and a modernized e-commerce platform, Baird Group is currently targeting a £100 million+ revenue milestone as it transitions into a service-first, omni-channel leader in the fashion sector.

Brooks Brothers seals record 2025 with $9 billion ‘Catalyst’ merger and NYC flagship expansion

The American sartorial landscape shifted decisively this year as Brooks Brothers announced record-breaking annual results alongside the strategic inauguration of its new global flagship. Under the leadership of Ken Ohashi, Brand CEO, the 207-year-old retailer has officially integrated into Catalyst Brands, a multibillion-dollar powerhouse formed by the landmark merger of Sparc Group and JCPenney. This alignment places Brooks Brothers within a massive retail ecosystem generating $9 billion in annual revenue, providing the legacy brand with the capital and logistical resources to accelerate its 2026 global expansion.

Flagship opening marks triumphant return to lower Manhattan

A central pillar of the brand’s resurgence is the opening of its NYC global flagship at 195 Broadway. Spanning nearly 10,000 sq ft within the historic former AT&T headquarters, the store bridges heritage with modern luxury, featuring a rotating exhibit of archival artifacts, including a replica of Abraham Lincoln’s inauguration coat. To capture a younger demographic, the retailer also launched the ‘University Shop,’ a collection designed to modernize Ivy League aesthetics. This physical push is yielding high returns; industry data indicates, the ‘New Preppy’ trend has driven a double-digit uptick in sales for tailored apparel as consumers trade fast fashion for archival investments.

The 125-year Oxford: Leveraging heritage for global scale Innovation remains tethered to tradition, evidenced by the global celebration of the 125th anniversary of the Button-Down Collar Oxford- a garment Brooks Brothers invented in 1900. Featuring icons like Selma Blair and Hasan Minhaj, the anniversary campaign has served as a powerful vehicle for storytelling, driving a surge in brand sentiment. As Marc Rosen, CEO, Catalyst Brands takes the helm, the focus moves towards omni-channel dominance. By leveraging a combined database of 60 million customers, Brooks Brothers aims to implement AI-driven personalization and unified loyalty programs, ensuring the ‘original American brand’ remains as technologically sharp as its tailored lapels.

America’s oldest clothing retailer, Brooks Brothers was founded in 1818 by Henry Sands Brooks with a commitment to fine craftsmanship. Credited with introducing the ready-to-wear suit and outfitting 40 US Presidents, the brand is a cultural cornerstone of American fashion. Now a key pillar of the Catalyst Brands portfolio, it operates over 500 global locations and specializes in premium menswear, women’s tailored clothing, and the iconic ‘Original Polo’ button-down. With record results in 2025 and a strategic shift toward high-traffic flagship experiences in markets like New York and Los Angeles, the brand is targeting sustained growth through a blend of heritage storytelling and modern lifestyle collaborations.

Bottega Veneta opens Gansevoort flagship as ‘Quiet Luxury’ outperforms in Manhattan

On December 13, 2025, Bottega Veneta officially inaugurated its new 3,358-sq-ft boutique at 58 Gansevoort Street, signaling a decisive shift in Manhattan’s luxury retail geography. Strategic proximity to New York’s fashion-forward cluster defines this expansion, as the Italian house joins prestigious neighbors like Hermès, Gucci, and Loro Piana in the Meatpacking District. This move reflects a broader trend identified in the 2025 JLL Luxury Retail Report, which noted a 65.1 per cent growth in new luxury square footage in New York during the first half of the year, with prime street-level locations commanding asking rents as high as $550 per sq ft.

Amidst a challenging climate for global conglomerates, Bottega Veneta remains a resilient outlier in Kering’s financial portfolio. While parent group Kering faced a 16 per cent revenue decline in H1 2025, Bottega Veneta emerged as a ‘rare bright spot,’ delivering a 3 per cent increase in comparable retail sales and double-digit growth in the North American market. "The house continues to assert its unique positioning through craftsmanship and retail exclusivity, even as the wider sector navigates structural headwinds," stated a Kering executive during the Q3 earnings call. As a case study in experiential and sustainable luxury, the Gansevoort boutique eschews traditional digital marketing in favor of a curated in-store library and the ‘Certificate of Craft’ program, which offers lifetime repairs. By prioritizing longevity and artistic dialogue over logo-centric trends, the brand successfully targets a discerning consumer base that is increasingly immune to ‘luxury fatigue.’

A premier Italian luxury house specializing in leather goods, ready-to-wear, and accessories. Bottega Veneta was founded in 1966 in Vicenza. The brand is the pioneer of the ‘When your own initials are enough’ philosophy, centered on its iconic Intrecciato leather-weaving technique. The house operates as a core subsidiary of the French group Kering, which acquired the brand in 2001.