"CMAI’s Apparel Index for Q2 July-Sept FY 2016-17 indicates the industry has recorded moderate growth with overall Index Value at 4.64 points compared to previous quarter (April-June FY 2016-17) when the overall Index Value was 5.45 points. However, in the same quarter last year, the Index Value had touched 6.68 points."

CMAI’s Apparel Index for Q2 July-Sept FY 2016-17 indicates the industry has recorded moderate growth with overall Index Value at 4.64 points compared to previous quarter (April-June FY 2016-17) when the overall Index Value was 5.45 points. However, in the same quarter last year, the Index Value had touched 6.68 points.

Large and Giant Brands, maintained their growth trajectory in Q2, which is still much higher than Small and Mid brands. Interestingly, unlike previous quarters, Large Brands fared better than Giant Brands in Q2. In fact, growth this quarter for Large Brands at 7.16 points is higher than last quarter’s 6.72 points but lower than the same quarter (8.95 points) previous year. The trend is different for Giant, Mid and Small Brands, as they performed much better last quarter compared to this quarter.

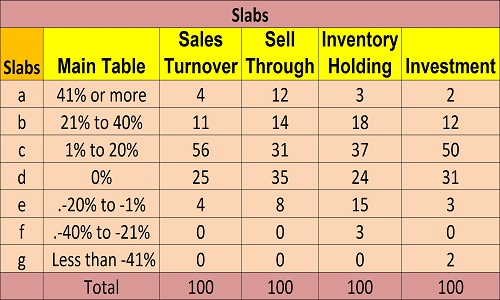

The overall Index value being restricted to 4.64 points, is mainly due to restricted increase in Sales Turnover (3.44 points compared to 3.92 points in the previous quarter), Sell Through (1.31 points over 1.69 points in the previous quarter) and Investments (1.42 points compared to 1.56 points in the previous quarter) relatively. However, Inventory Holding this quarter at 1.53 is better than 1.72 points of previous quarter. It may be noted that the lower value in inventory holding helps in the growth of index value.

Q2 Apparel Index growth slower that last quarter

CMAl's Q2 Apparel Index for the July-Sept (FY 2016-17) clocked in 4.64 points growth. This is approximately 32.19 per cent higher than the index for Small Brands (with turnovers of Rs 10 to 25 crores) which stood at 3.51 points. For Mid Brands (turnover of Rs 25-100 crores), growth is 5.35 points. They have performed much better than Small Brands. However, it’s the Large Brands that have led the growth story this quarter with 7.16 points that has grown the most, even higher than Giant Brands with an index value of 6.44 points. In fact, Large and Giant Brands have consistently being doing well. Notably, index value for Large Brands is 54.31 per cent higher than the Overall Index value.

The Index once again shows Large and Giant Brands are consistently doing better compared to Mid and Small ones. Small Brands have grown the least since positive attributes like Sales Turnover, Sell Through and Investments are dragging down growth and not contributing enough. However, overall Inventory Holding at 1.27 against 1.53 is better this quareter. Both Small and Large Brands have shown lower inventory holding than overall index. The index pattern like earlier quarters continues the trend, as size of the brands goes up from Small to Mid and from Mid to Large, but difference this time is it comes down from Large Brands to Giant Brands. Giant Brands at 6.44, have not performed as good as Large Brands at 7.16. Much higher Inventory Holding in case of Giant Brands at 3.44 against 1.41 for Large Brands, as well as lower growth in Investments in Giant Brands at 1.25 points comparing to 2.38 points for Large, are the two reasons for Giant Brands’ relative lower index value, in spite of having highest growth in Sales Turnover (6.00 points) and in Sell Through (2.63).

Large Brands fare better

What has worked in favour of Large Brands this quarter, having the highest index of 7.16 points that is 54.31 per cent higher than the Overall Index value, is mainly lower Inventory Holding at 1.41 and the highest Investments at 2.38 across all groups of different size of brands.

Generally, Q2 is known for EOSS period in the month of July, that boosts Sales Turnover but the next two months of August and Sept being pre-festive season months generally sales are not high. Higher Inventory Holding period specially in case of Giant Brands perhaps indicates that Giant Brands have been building inventories just before the festive seasons to achieve peak in sales on the back of buoyancy in spend by consumer during festive, winter and wedding seasons across the country.

Treading the tight rope between Sales Turnover, Inventory Holding

The correlation between Sales Turnover and Inventory Holding explains the difference in index value of different brand groups. A close look at Sales Turnover and Inventory Holding reveals that a cautious and tight control over inventories has an impact on the growth of sales turnover and hence the reason for index value not growing as much.

As the industry moves its learning curve over time, cautious inventories are restricting growth in general. As Rajeev Nair, CEO, Celio points out, “At Celio, we have kept a tight control on inventory over the last two years, we have seen progressive improvement in; End of Season’ inventory. We also work on progressive markdowns on slow movers so that season end inventory is limited. We have also started the practice of pilot stores where we test market new products as all fashion products don’t necessarily behave as we predict. Once successful, we roll across all stores. This increases our sell through rate.”

At the same time, especially indicated by few Giant Brands which have more focus on sales growth to tap opportunities during festive season, have been building higher inventories and infusing more Investments. Anant Daga, CEO, W and Aurelia says they increased investments as they saw an increase in Sales Turnover and improved Sell Through in the quarter, “Our brands W and Aurelia are expanding, products are being received well in the market and we are seeing good sale growth.”

For a winter focus products like thermals that have a narrow period of sales, inventory building is important, as Vinod Kumar Gupta, Managing Director, Dollar Industries, points out, “Some of our products i.e. thermals are seasonal in nature and production has done in the month of July and August. So, taking this into consideration our inventory is higher. But, since these products are seasonal in nature, it will be sold in the winter months. Which will lower our inventory and the closing stock will go down.” For Turtle on the other hand, the emphasis is on Sales Turnover keeping a close check on supply chain, Narendrra Parekh, Marketing Head, Turtle says, “We checked our supply chain management, keeping good fit and quality our major focus on products and refillment (replenishment) and last but not the least focus on marketing activities 360 degrees” have been the reasons for good performance.

Looking ahead to positive Q3

Around 65 per cent brands compared to 61 per cent in previous quarter feel the outlook for next quarter is ‘Good’, surely, a significant jump in outlook expectations. Another 17 per cent (previous quarter 19) brands say their outlook is ‘Excellent’ for the next quarter. Nearly 18 per cent, (same as last quarter), foresee an average outlook and no one feels (previous quarter 2) that it will be ‘Below Average’. Sept-Dec being a quarter for EOSS and the festive season, with Diwali falling in this period, may improve market sentiment, feel many brands, with a strong optimism. CMAl's Apparel Index CMAl's Apparel Index aims to set a benchmark for the entire domestic apparel industry and helps brands in taking informed business decisions. For investors, industry players, stakeholders and policymakers the index is a useful tool offering concrete and credible information, and is an excellent source for assessing the performance of the industry. The Index is analysed on assessing the performance on four parameters: Sales Turnover, Sell Through (percentage of fresh stocks sold), number of days of Inventory Holding and Investments (signifying future confidence) in brand development and brand building.