FW

Copenhagen GFA summit 2026 signals reset in global apparel finance

"

" The global apparel, textile, and fiber manufacturing industries are entering a decisive phase of financial and operational realignment, as senior executives, policymakers, and supply chain leaders gathered at the Global Fashion Summit 2026 in Copenhagen to confront growing systemic risks reshaping the sector. Held in the Danish capital of Copenhagen from May 5-7, the summit brought together more than 1,000 stakeholders under the theme ‘Building Resilient Futures’, with a clear consensus emerging: the industry’s existing capital allocation model is no longer compatible with the volatility of global production systems.

The discussions centred around the growing recognition that apparel supply chains are now exposed simultaneously to climate instability, geopolitical fragmentation, and rapid technological disruption. These forces are not operating in isolation but are compounding one another, creating what participants described as a permanently unstable operating environment. Against this backdrop, the sector’s traditional reliance on post-production correction mechanisms, markdown cycles, discount-driven inventory clearance, and marketing-led demand stimulation was widely criticized as unsustainable.

Rewiring capital flow in fashion

Instead, summit discussions emphasized the need for a fundamental reorientation of capital flows. Investment, leaders argued, must move away from downstream brand amplification and toward upstream industrial strength. This includes a renewed focus on material integrity, supply chain traceability, circular production systems, and workforce resilience in the face of automation. The shift represents not a marginal adjustment, but a restructuring of how value is defined and financed across the entire apparel ecosystem.

One important reframing emerged around the role of Chief Financial Officers, who were repeatedly described as the emerging ‘architects of resilience’. In this view, CFOs are no longer simply tasked with controlling costs or optimizing quarterly margins. Instead, they are increasingly responsible for determining the structural durability of entire production systems. Decisions around whether to fund material innovation, regional manufacturing capacity, or recycling infrastructure are now understood as strategic choices that directly influence long-term industrial survival.

Speakers argued that for decades, corporate capital allocation in fashion has disproportionately favored marketing expenditure and reactive inventory management over upstream investment. This imbalance has left core production systems undercapitalized, particularly in areas such as fiber development, textile processing, and tier-one manufacturing infrastructure. Even modest reallocations of capital toward these upstream segments, participants suggested, could materially stabilize margins that are increasingly under pressure from volatile energy prices, logistics disruptions, and fluctuating raw material costs. The underlying message was that brand strength cannot indefinitely compensate for weaknesses in physical production systems.

Climate shock and raw material exposure

This urgency is being increased by growing climate disruption across global fiber-producing regions. The upstream raw material base, once treated as a stable input layer, is now understood as one of the most exposed points in the entire value chain. Cotton cultivation, wool production, and synthetic fiber feedstocks are increasingly vulnerable to extreme weather events, agricultural stress, and ecological degradation. These disruptions are no longer isolated incidents but part of a broader structural trend reshaping agricultural reliability.

The scale of this disruption was underscored in data presented during the summit, highlighting the expanding footprint of climate-related shocks on textile supply systems.

Table: Global climate impact on textile supply chains in 2025

|

Metric |

Impact scale |

|

Climate-Related Disasters |

200+ major incidents recorded |

|

Population Affected |

87 million+ people globally |

|

Primary Crop Disruption |

Severe impacts on cotton harvests |

|

Manufacturing Interruptions |

Flood-related factory shutdowns |

|

Livestock Raw Materials |

Wildfires impacting wool regions |

The implications of this data extend beyond short-term supply volatility. Experts warned that failure to aggressively fund emissions reduction, ecosystem protection, and agricultural adaptation could push key production zones toward structural scarcity. In such a scenario, price volatility would be replaced by persistent supply insecurity, fundamentally altering how textile markets function. Participants emphasized that disruption is no longer an external shock to be managed but an internal condition of the system itself.

The missing circular economy infrastructure

Alongside climate risk, the summit also highlighted a critical gap in the global circular economy. While progress has been made in recovering industrial textile waste such as factory offcuts and surplus materials, post-consumer garment recycling remains extremely limited. Less than 1 per cent of discarded clothing is currently recycled back into new apparel production, revealing a significant gap between ambition and infrastructure.

The consensus was that this limitation is not primarily technological but structural. The circular economy, as several speakers noted, is not failing in principle it simply has not yet been built at scale. The missing component is industrial infrastructure capable of processing garments at commercial volumes and integrating recovered fibers into mainstream manufacturing systems.

This infrastructure deficit is compounded by the need for long-term, patient capital that individual brands are often unable or unwilling to deploy alone. As a result, calls intensified for coordinated public-private investment models capable of financing regional recycling ecosystems, from collection networks embedded in local communities to advanced fiber reprocessing facilities. Policy intervention was identified as essential to unlocking this transition, particularly through Extended Producer Responsibility (EPR) frameworks that assign end-of-life responsibility to brands and create financial incentives for circular design.

Automation and the human cost of efficiency

In parallel, the summit addressed the growing integration of artificial intelligence and automation into apparel manufacturing. While AI-driven systems are already improving design workflows, optimizing inventory planning, and increasing production efficiency, they also introduce significant disruption to labor markets, particularly in developing economies where most of the global fashion workforce is concentrated.

Automation in cutting rooms, pattern recognition systems, and quality control processes is delivering measurable productivity gains, but speakers warned that these gains are often reflected in corporate efficiency metrics without accounting for displaced labor. The human cost of this transition, they argued, is frequently externalized onto the very communities that underpin global textile production. As a result, there were strong calls for structured workforce transition programs, including large-scale upskilling initiatives and investment in hybrid human-AI production models designed to preserve employment pathways while modernizing operations.

Lessons from past industrial shifts

Historical context was also used to frame the current transformation. The industrialization of textile production during the Industrial Revolution fundamentally altered cost structures and accessibility. The post-war shift to ready-to-wear fashion democratized consumption in response to supply reconstruction. The digital revolution then reshaped distribution, branding, and consumer engagement by embedding commerce into digital ecosystems. Each of these transitions, participants noted, was driven by necessity rather than convenience, and each ultimately redefined the structure of the industry.

The current convergence of climate instability and artificial intelligence was positioned as the next comparable inflection point—one that will determine not only how fashion is produced, but whether its underlying systems remain viable under sustained stress.

As discussions concluded in Copenhagen, a unifying perspective emerged: the fashion industry is no longer optimizing for efficiency alone. It is now being forced to optimize for continuity. In this emerging paradigm, capital allocation is not merely a financial exercise, but a structural determinant of whether global apparel systems can remain functional under compounding environmental, technological, and geopolitical pressure.

United Textiles reports sharp revenue contraction in FY ’26

United Textiles has reported a significant financial downturn for FY26, registering a net loss of US $25.77 million. This performance stems from a nearly 60 per cent decline in operational revenue, signaling profound structural challenges within the company’s traditional manufacturing and distribution framework. The substantial drop in turnover highlights the firm's increasing difficulty in maintaining market relevance amid shifting global demand and intense competition from more agile, low-cost manufacturing hubs in the ASEAN region.

Navigating operational instability and market pressures

The company’s fiscal results reflect a broader pattern of volatility currently impacting mid-tier textile producers. Rising raw material costs, combined with the softening of orders from traditional North American and European retail partners, have severely constrained operating margins. To mitigate these pressures, industry analysts suggest the firm must undergo immediate operational restructuring to align its output with the burgeoning demand for sustainable and technically advanced textiles. The current loss indicates that the previous business model, heavily reliant on high-volume, commodity-grade production, is no longer sustainable under the current global trade environment, which increasingly rewards value-added innovation and speed-to-market capabilities.

Sectoral challenges and future viability

United Textiles’ struggles underscore the wider necessity for technological upgrades within legacy textile firms. As global retail majors increasingly demand end-to-end digital traceability and compliance with stringent environmental standards, companies failing to modernize their production floors face rapid obsolescence. The path toward recovery will likely necessitate a fundamental reassessment of the company’s product portfolio, shifting focus toward high-margin technical fibers and functional apparel. Without a decisive transition toward modernized manufacturing and a more diversified market strategy, the firm risks further erosion of its competitive standing in an industry that now prioritizes sustainability and supply chain transparency as foundational requirements for long-term contract security.

Producer of basic apparel and fabrics

United Textiles is a long-standing garment manufacturer and textile processor producing basic apparel and fabrics. Historically focused on mass-market exports to North American retailers, the company is currently facing severe financial distress. Management is evaluating restructuring plans to address dwindling revenues and restore operational efficiency amid intense global competition.

Supply chain bottlenecks stifle textile production

The Indian textile and apparel sector is currently grappling with significant operational disruptions as critical yarn shipments remain marooned at major ports. Industry analysts estimate, the value of stranded consignments has reached approximately US$26 million, directly threatening production timelines for garment exporters. These logistics hurdles stem from intensified customs scrutiny and procedural backlogs that have disproportionately affected small and medium-sized manufacturers who operate on thin inventory buffers. As domestic manufacturers struggle to secure essential raw materials, the cost of production is mounting, potentially eroding the global price competitiveness of Indian-made apparel.

Strategic implications for export competitiveness

Industry stakeholders are increasingly concerned, prolonged delays could force manufacturers to miss critical seasonal shipment windows for international retailers. Experts suggest, to mitigate these disruptions, firms must shift toward localized sourcing strategies or invest in advanced inventory management systems to buffer against supply chain volatility. According to Rajesh Mehta, Industry Consultant, the current logistical friction serves as a wake-up call for the sector to diversify its supply routes and enhance coordination with port authorities to streamline clearance processes. Without rapid intervention to unclog these entry points, manufacturers risk losing contract reliability in a tightening global market that demands both speed and cost-efficiency.

Operational overview of Indian textile manufacturers

Indian textile and apparel manufacturers specialize in the production of cotton, synthetic fibers, and value-added garments for global and domestic consumption. The sector remains focused on expanding its presence in high-growth markets like the United States and the European Union through sustained investment in sustainable manufacturing technologies and infrastructure improvements.

Customs duty waiver to revitalize textile value chain: AEPC

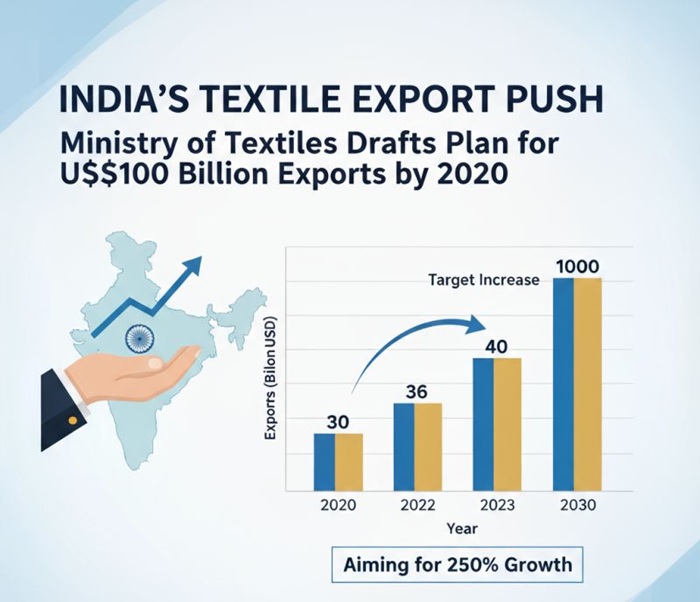

The Union Finance Ministry has implemented a temporary suspension of all customs duties and associated agricultural cesses on cotton imports, effective from June 1, 2026, through October 30, 2026. This policy intervention arrives at a critical juncture for the Indian textile and apparel sector, which has been grappling with a supply-demand deficit estimated at approximately 45 lakh bales for the 2025-26 season. By removing the 11 per cent effective duty burden, the government aims to mitigate the inflationary pressures that have constrained production margins for domestic manufacturers, particularly within the MSME segment.

Strengthening global export competitiveness

Industry stakeholders, including the Apparel Export Promotion Council (AEPC), have characterized the waiver as a vital corrective measure to restore India’s price parity with regional competitors such as Bangladesh and Vietnam. This timely intervention is essential to stabilize the value chain and empower garment exporters to fulfill international orders with greater margin flexibility, notes Dr A Sakthivel, Chairman, AEPC. The industry has urged spinning mills to ensure these cost efficiencies are passed downstream, thereby rationalizing yarn prices. As India pursues an ambitious $100 billion export valuation by 2030, this duty-free window is expected to provide the operational buffer required to leverage recent Free Trade Agreements (FTAs) and expand market share in key destinations, including the UAE and European markets.

A foundational pillar of the national economy

The Indian textile and apparel industry serves as a foundational pillar of the national economy, encompassing the full value chain from fiber production to finished garments. Key export categories include ready-made garments, cotton yarn, and home textiles. The sector is currently prioritizing modernization and sustainable production to secure large-scale global contracts.

Hellmann and MAS Holdings expand apparel logistics capabilities in Sri Lanka

To address the increasing complexity of global garment supply chains, Hellmann Worldwide Logistics and MAS Holdings have expanded their collaborative infrastructure with a specialized fashion-focused distribution hub in Sri Lanka. This facility is engineered to provide end-to-end supply chain visibility for international apparel brands, integrating advanced inventory management systems to mitigate delays in raw material procurement and finished goods dispatch.

Enhancing velocity in fashion retail

The strategic deployment of this hub serves as a critical response to the shortening lead times demanded by global retail giants. By locating logistics operations in closer proximity to manufacturing clusters, the partnership aims to significantly reduce dwell times for high-volume apparel orders destined for North American and European markets. This operational enhancement is essential for brands transitioning to ‘fast-fashion’ replenishment cycles, where speed-to-market is a primary competitive advantage. The facility emphasizes multi-channel fulfillment, supporting both wholesale distribution and direct-to-consumer logistics, thereby providing a flexible framework for retailers navigating unpredictable market demand.

Strengthening regional trade resilience

As global apparel brands prioritize de-risking their supply networks, the new hub functions as a stable node for sustainable and compliant logistics. By streamlining the flow of technical textiles and high-value garments, the initiative provides a robust buffer against regional trade fluctuations. Industry analysts note, such infrastructure is paramount for Sri Lanka to maintain its position as a preferred sourcing partner for global labels, especially as brands increasingly demand end-to-end digital product traceability. This integration of logistics and manufacturing efficiency is expected to improve cost structures, allowing both companies to scale operations as demand for regional manufacturing intensifies.

Logistics and manufacturing partnership

A leading global apparel manufacturer based in Sri Lanka, MAS Holdings specializes in intimate wear and high-performance activewear. Hellmann Worldwide Logistics provides global supply chain solutions, including fashion-specific logistics and freight management. Together, they streamline the movement of goods from manufacturing floors to global retail distribution centers.

Express Inc navigates complex restructuring following Chapter 11 filing

The apparel sector is witnessing a significant consolidation as Express Inc, the prominent specialty retailer, undergoes a comprehensive restructuring. Following the judicial oversight of its Chapter 11 proceedings, the company is executing a definitive store rationalization plan to stabilize its balance sheet. This initiative involves the permanent closure of numerous underperforming retail locations across the United States, a measure necessitated by sustained declines in physical store traffic and the failure of recent turnaround strategies to resonate with target consumers. Management is currently prioritizing the streamlining of its operational cost structure, seeking to exit high-overhead leases that have disproportionately impacted margins throughout the previous fiscal cycles.

Transitioning toward a sustainable omnichannel future

The restructuring mandate extends beyond physical contraction; it encompasses a broader realignment of the company’s inventory management and digital commerce architecture. By consolidating its retail presence, Express Inc aims to shift resources toward boosting its online platform and improving the efficiency of its remaining omnichannel touchpoints. Industry analysts have noted the brand’s inability to capture Gen Z market share, coupled with intensifying competition from fast-fashion disruptors, has underscored the urgency of this transformation. As the company continues to navigate these financial complexities, the overarching focus remains on achieving long-term solvency through a leaner, more agile business model that prioritizes profitability over expansive physical distribution.

Offering modern styles for work and leisure

Express Inc. is a specialty retailer offering fashion apparel and accessories for women and men. It focuses on modern, versatile styles suitable for work and leisure. Following recent financial headwinds, the company is undergoing a major restructuring to rationalize its store footprint, enhance digital capabilities, and improve overall operational profitability.

Tech giants and couture: The new economic synergy

Silicon Valley is currently reconfiguring its corporate identity, moving away from utilitarian aesthetics toward a sophisticated ‘taste economy.’ Characterized by the emergence of ‘taste-washing,’ this shift sees major technology firms integrating high-fashion sensibilities and curated artisanal collaborations into their brand portfolios to cultivate cultural capital.

Leveraging cultural capital through apparel

The strategy extends beyond mere executive appearances at international fashion weeks. Corporations are increasingly releasing proprietary apparel lines, such as Palantir’s high-demand, domestically manufactured chore coats, which frame complex software services within the narrative of American industrial heritage. By adopting the visual language of heritage brands, these organizations aim to soften their corporate image, presenting technology through a lens of craftsmanship and human-centric design. Industry analysts suggest that this trend signifies a move towards branding that prioritizes aesthetic values as a proxy for corporate trustworthiness, essentially transforming fashion into a strategic instrument of public relations and brand positioning.

Bridging the gap between concept and consumer

This convergence of sectors arrives at a time when traditional couture is simultaneously questioning its own relationship with the wearer. The recent debate at the 2026 Cannes Film Festival regarding the functionality of conceptual garments highlights a growing industry preference for design that balances narrative impact with ergonomics. As tech companies invest in highly curated aesthetics, the apparel sector faces a unique opportunity to provide the "cultural fluency" these giants seek. The challenge for established retail brands is to maintain their authenticity as they compete for attention in a marketplace where software developers are now influencers in the front row. Successful integration will require apparel firms to provide high-concept garments that remain accessible, ensuring that the spectacle of fashion does not overshadow the necessity of the wearer’s comfort and utility.

The emergence of the taste economy

The taste economy represents the strategic alignment of technology firms with high-end fashion and art to enhance brand perception. Key sectors include curated apparel, luxury experiences, and high-quality merchandising. Companies are utilizing these initiatives to drive market penetration among Gen Z and millennial demographics while shifting the public discourse from corporate utility to cultural relevance. This phenomenon is currently reshaping traditional retail partnerships and setting a new benchmark for brand identity in the AI era.

Strategic cotton duty waiver boosts Indian textile export competitiveness

In a significant move to stabilize the domestic apparel value chain, the Union Finance Ministry has exempted cotton imports from customs duties and associated agricultural cesses for a five-month window, effective June 1, 2026. This intervention addresses critical supply-side bottlenecks that have hampered the sector’s global price competitiveness, particularly against regional rivals in Bangladesh and Vietnam who benefit from duty-free raw material access.

Addressing cost volatility in global markets

Accounting for approximately 8 per cent–10 per cent of India’s total merchandise exports, the textile and apparel industry has faced significant headwinds due to fluctuating raw material prices and softening global demand. Government data indicates, total textile and apparel exports reached $35.79 billion in FY26, a 2.2 per cent decline from the previous fiscal year. Industry leaders, including the Confederation of Indian Textile Industry (CITI), have consistently highlighted that high import duties on long-staple cotton—sourced primarily from the US, Egypt, and Australia - were impeding India's ability to maintain thin margins in the highly price-sensitive international apparel trade. By removing the 11 per cent effective duty burden until October 31, 2026, the government aims to lower production costs for small and medium enterprises (MSMEs) and improve the global standing of Indian manufacturers.

Leveraging new trade frameworks

Beyond domestic policy support, the sector is capitalizing on a diversification strategy to mitigate regional trade volatility. While traditional markets like the US remain central, significant growth has been observed in newer destinations such as the UAE, Germany, and Spain, where Indian exports have seen double-digit increases. The operationalization of the India-Oman Comprehensive Economic Partnership Agreement (CEPA) on June 1 serves as a strategic pivot to further diversify market reach. According to industry analysts, these duty-free avenues, combined with the temporary cotton relief, provide a much-needed operational buffer.

As India pushes toward a $100 billion export target by 2030, the focus is shifting toward value-added production - such as performance-treated, sustainable, and technical textiles—which now command a premium in European and North American markets.

A comprehensive value chain

The Indian textile industry is a comprehensive value chain covering fiber production, spinning, weaving, and garment manufacturing. Major export categories include ready-made garments, cotton yarn, and home textiles. The sector currently prioritizes modernization and sustainable, compliant manufacturing to secure long-term contracts with global retail majors.

India-Oman trade pact opens new avenues for textile exporters

Having officially entered into force on June 1, 2026, the India-Oman Comprehensive Economic Partnership Agreement (CEPA) marks a transformative chapter for the domestic textile and apparel sector. By eliminating the prevailing 5 per cent import duties on various textile products, the agreement provides Indian manufacturers with an immediate competitive advantage in a region that serves as a vital logistics gateway for the broader Gulf, East African, and Middle Eastern markets.

Strategic market integration

India is rapidly solidifying its footprint in the Omani textile market. Recent data underscores this momentum, with India’s share of Oman’s total textile imports rising from 9.3 per cent in 2023 to approximately 22 per cent in 2024. As bilateral trade reached $11.18 billion in the FY25-26, the CEPA is expected to further catalyze this growth. Industry stakeholders view the deal as a critical structural shift, particularly for the readymade garments, made-ups, and man-made fiber segments, which have historically faced price sensitivity in the Gulf. This agreement provides the necessary fiscal relief for our MSMEs to achieve greater scale and integration within global value chains, noted a senior official from the Ministry of Commerce.

Logistics and supply chain resilience

Beyond tariff reductions, the partnership positions Oman as a strategic hub for Indian exports, leveraging ports such as Sohar and Salalah to mitigate risks associated with regional maritime volatility. For apparel exporters, the ability to bypass traditional bottlenecks by utilizing these out-of-Strait ports offers a more resilient supply chain architecture. Exporters are now encouraged to utilize the Trade Connect portal to secure preferential Certificates of Origin, ensuring that shipments transition smoothly under the new zero-duty framework. As India targets a $100 billion textile export valuation by 2030, this integration with the Omani market serves as a blueprint for diversifying reach beyond conventional Western destinations.

A cornerstone of the national economy

The Indian textile and apparel industry encompasses the entire value chain from fiber production to finished garments. The sector remains a cornerstone of the national economy, prioritizing exports to the US, EU, and Middle East. Current growth strategies emphasize product diversification, sustainable manufacturing, and deeper penetration into FTA-enabled markets to maintain global competitiveness.

Global apparel supply chains realign as India navigates trade volatility

The global apparel and textile sector is experiencing a significant structural shift, as major manufacturers and retailers move away from traditional, single-source dependency in favor of multi-country footprints. Much like the consumer goods industry recently de-risked its logistics by moving operations to mitigate regional instability, apparel firms are now aggressively rerouting supply chains to navigate tariff shocks, raw material volatility, and shifting geopolitical landscapes.

Redrawing the global textile map

The current landscape is characterized by a strategic departure from centralized production. Major exporters are increasingly reassigning US-bound production orders to more favorable geographic hubs. For instance, Pearl Global Industries has reported growing demand for its operations in Vietnam, Indonesia, Bangladesh, and Guatemala, highlighting a deliberate movement of capacity to locations that offer better trade access or cost efficiencies. Similarly, other top-tier exporters are leveraging manufacturing bases in Africa to insulate their North American supply chains from potential disruptions. This transition reflects a broader “China plus one” strategy, now evolving into a more complex, diversified portfolio approach as global buyers prioritize supply chain resilience over singular cost advantages.

Strengthening domestic competitiveness

In response to these global pressures, the Indian government and industry leaders are implementing a dual-track strategy focused on both raw material security and long-term cost optimization. To address domestic input cost spikes, the Finance Ministry recently waived the 11 per cent import duty on cotton, effective from June 1 through October 30, 2026. This intervention is designed to ensure adequate raw material availability for the textile industry, particularly for MSMEs, and to stabilize costs after cotton prices experienced significant fluctuations, previously spiking to Rs 71,000 per candy.

Furthermore, the government is currently developing a comprehensive cost roadmap to align India’s textile ecosystem with international benchmarks. By mapping raw materials, compliance standards, and taxation frameworks, the initiative aims to close the competitiveness gap. Industry bodies are actively lobbying to increase the Remission of State and Central Taxes and Levies (RoSCTL) benefits to 10 per cent, a move viewed as essential to achieving parity with the duty-free advantages enjoyed by manufacturers in Bangladesh and Vietnam.

Challenges and future outlook

While India targets a $100 billion export valuation by 2030, the path forward requires addressing structural hurdles. Data indicates, labor productivity in India remains 20 per cent to 40 per cent lower than that of key competitors, and the nation currently holds only a 6 per cent share of the $107.7 billion US textile import market.

However, the outlook remains cautiously optimistic. As labor costs rise in Vietnam and political instability creates uncertainty in other manufacturing hubs, India is positioning itself as a reliable, balanced growth destination. By tapping into strategic trade agreements with the UK, Japan, and Australia, Indian manufacturers are moving beyond traditional reliance on the US market. The consensus among industry stakeholders is that the current period represents a watershed moment; in the 2026 trade environment, supply chains are no longer snapping—they are effectively rerouting, and India is positioning its manufacturing base to capture the resulting long-term value.