![]()

FW

To forge a unified state-central roadmap for industrial scaling, the Ministry of Textiles is convening the National Textiles Ministers’ Conference in Guwahati on January 8–9, 2026. This summit is being held as the federal government extends the Production Linked Incentive (PLI) Scheme application window to March 31, 2026, signaling an urgent push to fill the manufacturing vacuum in Man-Made Fiber (MMF) and technical textiles. The strategic objective is to synchronize regional policies with the national target of achieving US$ 100 billion in exports and a total market size of US$ 350 billion by 2030.

Enhancing global competitiveness through MMF and technical textiles

A primary focus of the Guwahati deliberations is the structural transition toward high-growth segments like MMF and functional fabrics. While India currently dominates the global cotton yarn market, it lags in the weaving and processing stages where China and Vietnam maintain a cost advantage. To counter this, the government is incentivizing large-scale integrated infrastructure through the PM-MITRA parks. Recent data indicates, India’s textile exports grew by 5.37 per cent in mid-2025, reaching US$ 3.10 billion monthly, yet officials emphasize that achieving the 2030 targets requires a sustained 15 per cent-20 per cent growth rate.

Unlocking the North-East textile corridor

The conference includes a dedicated conclave aimed at transforming North-East India into a specialized hub for sustainable and high-value textiles. By focusing on bamboo-based fibres, Muga silk, and handloom-driven women’s enterprises, the Ministry intends to brand ‘Textiles from North-East’ as a premium global category. This initiative is about integrating regional craftsmanship with global value chains to ensure our traditional heritage meets modern technical standards, states a senior official. The integration of sustainable practices and green chemistry is expected to be a key differentiator for Indian apparel in ESG-compliant Western markets.

Policy framework and sectoral objectives

The Ministry of Textiles oversees the entire value chain from fibre production to retail. Current growth plans involve operationalizing seven PM-MITRA parks and leveraging the Rs 10,683 crore PLI scheme to boost MMF output. Financially, the sector contributes 2.3 per cent to India's GDP, with a roadmap to triple current export volumes by 2030.

In South Korea, China, and the United States, clothing retail sales have maintained year-on-year growth, driven by each country's economic stimulus measures. As apparel inventories decrease, there is analysis suggesting that the stock prices of textile and apparel-related companies, which have bottomed out, could rebound.

On January 2, Shinhan Investment Corp. maintained its overweight recommendation on the textile and apparel sector, citing these factors. The firm selected Youngone Corporation as its top pick, while also highlighting F&F, Gamsung Corporation, and AU Brands as stocks to watch.

From the second half of last year through November, the clothing retail sales growth rate in South Korea, China, and the United States averaged around 3 per cent Y-o-Y. Certain segments, such as women's apparel, saw growth rates reaching the low double digits. Notably, apparel inventory levels in both South Korea and the United States are currently at their lowest points in the past three years, fueling expectations for increased shipments.

In South Korean department stores, women's apparel has maintained around 5 per cent Y-o-Y sales growth since June of last year. Casual wear, men's clothing, and children's and sports apparel also saw department store sales growth throughout the second half of the year, except for September. While the luxury segment continued to post sales growth in the low double digits, deepening consumption polarization, it is noteworthy that department store apparel sales have grown for five consecutive months for the first time in two years since 2023, which is seen as an encouraging sign.

Having outperformed the market in sales growth during the second and third quarters of last year, Gamsung Corporation is estimated to have achieved sales growth exceeding 20 per cent Y-o-Y from October to early December. Similarly, clothing retail sales in China are estimated to have grown by 3-5 per cent Y-o-Y in the second half of last year. With the base effect expected to be pronounced through the first half of this year, China's clothing retail sales are anticipated to maintain their growth momentum for the time being. This is why attention is being paid to companies such as F&F, Gamsung Corporation, and AU Brands, which are planning to expand into China this year.

The reduction in inventory is also a positive signal. Recently, apparel inventory levels in the United States have remained at the lower end since 2023. The report emphasized that attention should be paid to the potential for earnings recovery among original equipment manufacturing (OEM) companies this year. However, it remains uncertain whether American consumers will maintain their purchasing power in the face of inflation driven by tariffs. Lagging indicators that could confirm this are expected to emerge after the first quarter of this year, but until then, investment sentiment may be concentrated on OEM companies.

Park Hyunjin, a researcher at Shinhan Investment Corp, stated, Youngone Corporation's investment appeal may further increase, as its sales are expected to grow significantly due to benefits from certain clients, even though its correlation with consumer sentiment is low. ‘This presents an opportunity for its price-earnings ratio (PER) multiple to expand, he added.

Luxury fashion availability in Russia has entered a new phase of logistical complexity as the market adapts to the EU’s expanded export prohibitions. Despite a formal ban on European luxury goods with wholesale values exceeding €300, iconic labels including Gucci, Burberry, and Dolce & Gabbana remain prominently featured in Moscow’s flagship department stores. However, the cost of circumvention is being passed directly to the consumer. A comprehensive price audit of 600 luxury items at TSUM reveals, Russian shoppers are currently paying an average of €2,626 for goods that retail for €1,229 in Paris or Milan - a staggering 113 per cent premium.

Logistics arbitrage and third-country rerouting

The persistence of European apparel and accessories is underpinned by a sophisticated network of ‘parallel imports’ and personal shopping intermediaries. Customs data from the first quarter of 2025 indicates,major Russian distributors are successfully sourcing high-value inventory via Turkey, the United Arab Emirates, and China. While direct shipments from the EU are strictly limited to lower-priced "entry-level" luxury items to remain compliant with the €300 threshold, boutique agencies like Global Style Import are declaring high-end silk dresses and leather bags at significant markups after transshipment through neutral hubs.

The rise of the status premium

This bifurcated supply chain has transformed the Russian luxury landscape into a ‘status-for-scarcity’ model. While mid-market brands struggle with a 2.8 per cent decline in real disposable income, the ultra-wealthy demographic remains relatively price-inelastic. Investors are closely monitoring how this ‘sanctions tax’ affects the broader apparel sector, which saw a 4.3 per cent reduction in physical store counts by mid-2025. Paradoxically, the high cost of acquisition has only served to reinforce the exclusivity of Western brands, even as domestic manufacturers and Iranian leather labels attempt to capture the resulting market vacuum.

Mercury Fashion, Russia’s premier luxury distributor since 1993, operates the TSUM department store and various high-end boutiques. Despite geopolitical headwinds, it maintains a robust digital presence and 95 per cent in-store conversion rates. The firm is currently leveraging a ‘compliant direct-import" model for accessories while utilizing third-party logistics for heritage couture.

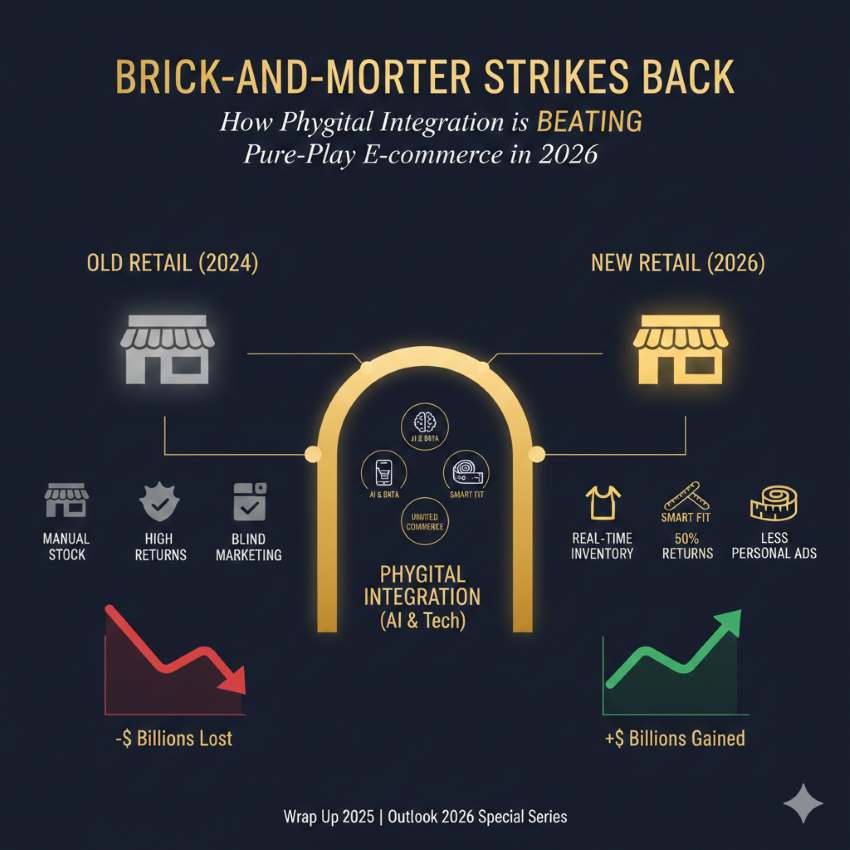

The American retail landscape underwent a seismic restructuring in 2025, defined by the collapse of legacy fast-fashion icons under the weight of ‘ultra-fast’ digital competition. Data from Coresight Research confirms, roughly 8,200 stores shuttered nationwide last year - a 12 per cent rise from 2024 - marking the highest level of retail volatility since the pandemic. The most striking casualty was Forever 21, which wound down all US operations after failing to defend its mall-based empire against the aggressive pricing of cross-border e-commerce giants.

The pricing chasm and the de minimis shift

Strategic missteps in physical site selection were exacerbated by a pricing war Forever 21 could not win. While the brand struggled with rising domestic labor costs and brick-and-mortar overhead, overseas competitors like Shein and Temu leveraged a $100 billion global scale to capture cost-conscious Gen Z shoppers. However, the sector faces a new turning point in early 2026 as the federal government eliminates the ‘de minimis’ trade exemption. This policy shift, which previously allowed duty-free entry for packages under $800, is expected to drive up import costs for digital retailers, potentially offering a slim window of opportunity for surviving domestic apparel brands.

Shifting toward experience and value

As discretionary spending on durable goods is projected to rise by 4.7 per cent in 2026, the industry is witnessing a ‘Great Retail Reset.’ Legacy survivors are moving away from the high-volume, low-quality model that doomed Forever 21. Retail analysts note a decisive trend toward ‘phygital’ strategies - merging interactive in-store experiences with seamless digital fulfillment. The retailers that will thrive are those who view their physical footprint as a strategic advantage rather than a liability, noted one industry CEO. With inflation easing to 2.3 per cent, the focus is now on justification of price through quality, as consumers trade blind brand loyalty for tangible value and sustainability.

Retail restructuring and legacy management

Forever 21 was a Los Angeles-based fast-fashion pioneer that once operated 800 global stores. Following its 2025 liquidation, its brand intellectual property remains under Authentic Brands Group. The company is now exploring a digital-only licensing model to service international markets while exiting high-cost US physical real estate entirely.

In a decisive shift for Bangladesh's textile landscape, the interim government has officially scrapped a direct deal with Japanese firm Revival Group, opting instead for an open international tender to lease the debt-stricken Beximco Industrial Park.

Overseen by the Bangladesh Investment Development Authority (BIDA) on the directives of Muhammad Yunus, Chief Adviser this transition aims to uphold public procurement transparency. The pivot follows an impasse where state-owned Janata Bank and the Financial Institutions Division failed to reach a consensus on the previous tripartite draft, citing the lack of competitive bidding as a primary concern.

Lender aggression and asset auctions

The urgency for a new operator is fueled by a staggering default profile exceeding 35,000 crore BDT ($2.9 billion). Janata Bank, which holds nearly 65 per cent of this exposure, recently initiated independent auction processes for key units including International Knitwear & Apparel and Urban Fashions. While a recent High Court stay has temporarily paused these sales, the bank continues to push for aggressive recovery. The primary goal is the immediate recovery of the 600 crore BDT government loan used for worker arrears, stated M Sakhawat Hossain, Brigadier General (retd), Potential lessees must now demonstrate not only operational expertise but also the capacity to satisfy the state's priority claims.

Operational survival and export viability

Despite the financial turmoil, Beximco’s 15 textile units remain a high-value asset due to advanced machinery and a legacy of servicing global majors like Inditex and Target. The industry view, echoed by BGMEA leadership, suggests, successful leasing depends on a ‘reputation-first’ operator who can restore buyer confidence shattered by the February shutdown. Any new contract will likely reflect the original proposal’s core structure: the operator provides working capital while profit shares are funneled directly to debt adjustment, bypassing the original owners.

The BIDA-led leasing initiative targets the revitalization of 15 garment and textile factories at the Beximco Industrial Park in Gazipur. Focused on high-capacity apparel exports, the plan seeks to reinstate 25,000 workers while servicing a 23,000 crore BDT debt to Janata Bank. Management under the new tender will focus on technical efficiency and ESG compliance to regain international brand certification.

The premium fashion house LK Bennett, a perennial favorite of high-profile figures like the Princess of Wales, has initiated high court proceedings to appoint administrators. This move, executed on December 30, 2025, signals a potential second collapse in six years for the 35-year-old retailer. Despite intensive efforts by its current owners, Byland UK, to secure emergency financing throughout the fourth quarter, the brand has struggled to navigate a volatile consumer landscape characterized by high household savings rates and a 2.8 per cent decline in real disposable income.

Structural pressures on mid-market luxury

The brand’s financial health has deteriorated significantly over the last fiscal cycle. For the period ending January 2024, LK Bennett reported post-tax losses of £3.2 million on a turnover that plummeted to £42.1 million - a sharp 14 per cent decrease from the previous year. Auditors from Grant Thornton had previously identified a ‘material uncertainty’ regarding the company's status as a going concern, particularly after it breached debt covenants involving a £22 million borrowing pile. The upcoming February 2026 deadline for debt renegotiation acted as a final trigger for the administration filing.

Industry-wide insolvency contagion

LK Bennett’s distress mirrors a broader malaise within the UK’s ‘textiles and clothing’ sub-sector, which was labeled a primary ‘market loser’ in 2025 by industry analysts. Mounting operational costs, including the recent hike in National Insurance contributions and the phasing out of pandemic-era business rate reliefs, have squeezed margins to breaking points. While luxury rivals like Cartier have shown resilience, mid-tier premium labels are increasingly caught between high-street price sensitivity and the rising costs of maintaining prime physical footprints in London and Jersey.

Strategic retrenchment and heritage

Founded in 1990 by Linda Bennett to bring ‘Bond Street to the High Street,’ the brand has transitioned from 200 global outlets to just nine standalone UK stores. Current growth plans are stalled as the business seeks a buyer capable of servicing its debt while pivoting toward a digital-first wholesale model.

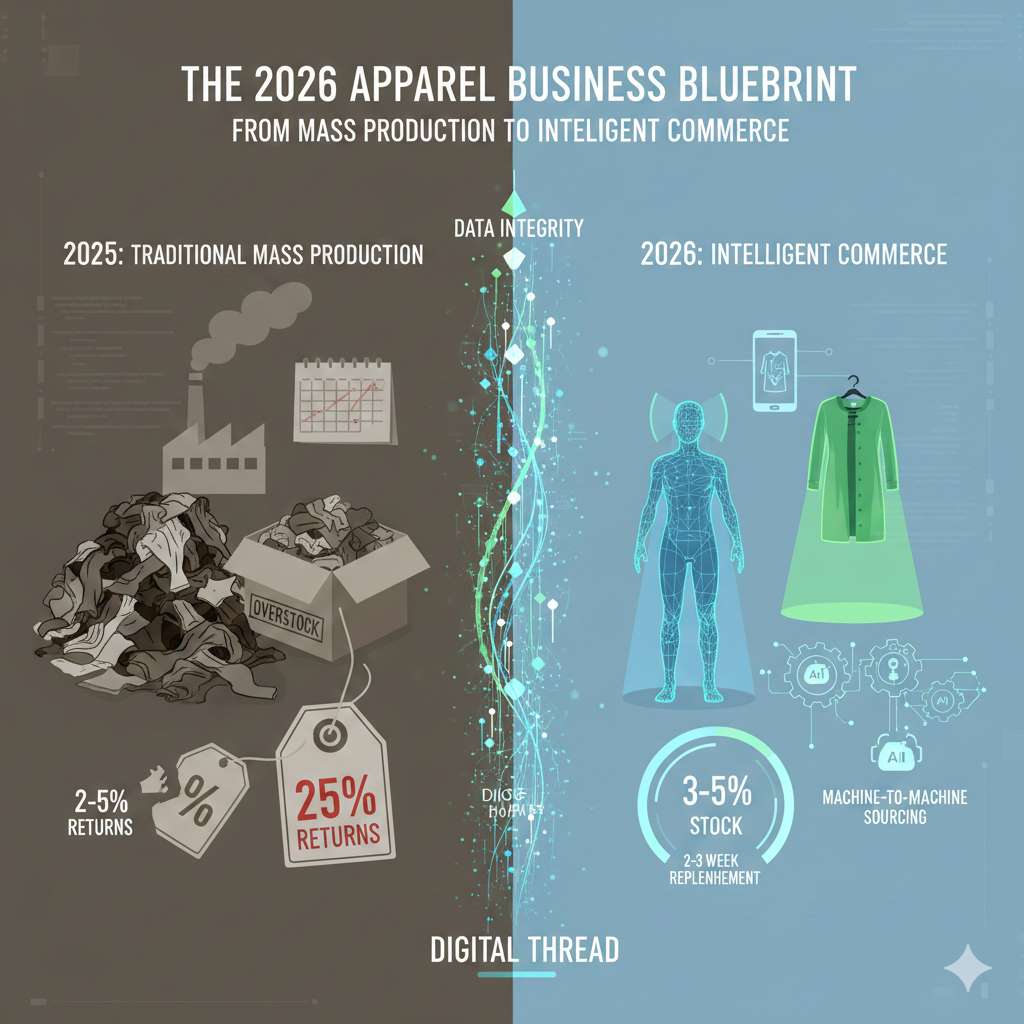

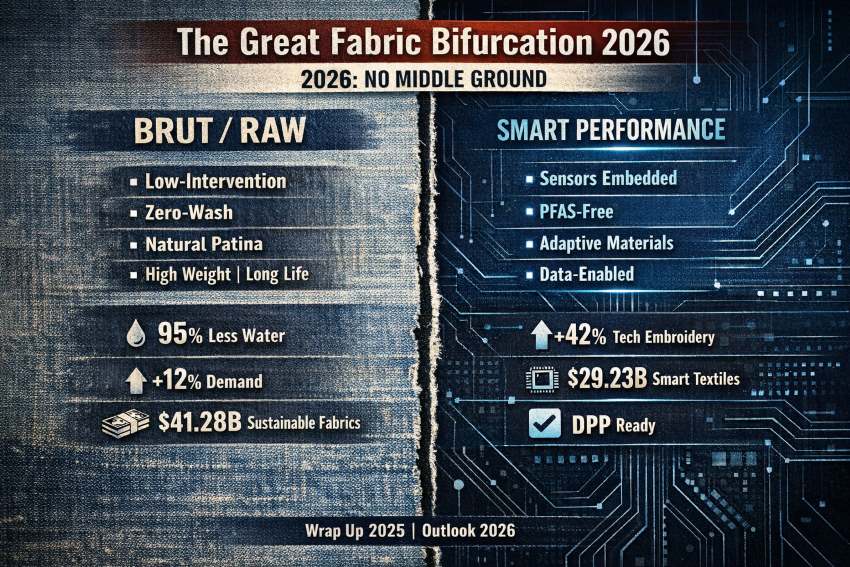

As part of our definitive annual series, "Wrap Up 2025, Outlook 2026," we examine how the textile and apparel sector has moved beyond a phase of simple recovery into a period of high-stakes material evolution. The final data from 2025 reveals an industry no longer satisfied with singular product identities. Instead, we are entering 2026 in a state of productive tension, a "Great Bifurcation" where the commercial appetite for raw, unadulterated "Brut" authenticity is matched only by a capital-intensive surge in high-tech, intelligent performance textiles. For the C-Suite, the strategic mandate of 2026 is clear: market leadership now requires a dual-track mastery of both artisanal heritage and technological developments.

The "Brut" revolution of late 2025 emerged as a direct commercial response to decades of chemical over-processing. In the denim sector, the move toward unwashed, untreated "Raw" or "Brut" fabrics has transitioned from high-end boutiques to global sourcing schedules. This aesthetic is the cornerstone of a broader movement toward Sustainable Fabrics, which have evolved from a niche preference to a $41.28 billion powerhouse. In 2026, the definition of sustainability has expanded to include "Low-Intervention" textiles—materials that emphasize their natural state through reduced scouring, bleaching, and finishing. Retailers in major import markets reported a 12% increase in demand for these rigid, high-weight textures as consumers favor garments that offer a personal patina and long-term durability. This is a high-margin sustainability play; by eliminating traditional stone-washing and chemical distressing, "Brut" production reduces factory water consumption by up to 95%.

Running parallel to this raw aesthetic is the rapid industrialization of bio-based and regenerated fibers. The global sustainable fabric market is projected to reach $134.7 billion by the end of 2026, driven by a 12% CAGR in organic and recycled segments. We are seeing a massive shift toward "Circular Feedstocks," where agricultural waste is transformed into high-performance cellulose. This is not merely an environmental choice but a regulatory necessity; as we head into 2026, the market value of recycled polyester is expected to hit $10 billion, reflecting its role as a primary substitute for virgin synthetics.

Simultaneously, the "Smart Performance" segment is capturing a larger share of global R&D budgets. Driven by a 42% surge in the technical embroidery market, where conductive threads are integrated directly into the fabric base, the 2026 outlook for intelligent textiles has moved from experimental labs to the mainstream supply chain. We are seeing the commercialization of "Opaque Rainproof" materials that utilize biomimicry to repel water without the use of restricted PFAS chemicals. Even in high-fashion categories, a 20% rise in demand for fine lace in the EU is being supported by the integration of high-tenacity, "invisible" synthetic fibers to ensure these delicate aesthetics meet the rigorous durability requirements of the upcoming 2026 circularity mandates.

2026 sectoral growth & performance forecast

The move into 2026 is defined by a massive reallocation of capital toward materials that satisfy the "Double Agenda" ; fabrics that deliver high-performance functionality while maintaining full compliance with the EU Digital Product Passport (DPP) registry, which becomes operational in mid-2026.

|

Fabric Segment |

2025 Market Value (Est) |

2026 Revenue Forecast |

Key Innovation Driver |

|

Sustainable Performance |

$37.26 Billion |

$41.28 Billion |

PFAS-free Hydrophobic Coatings |

|

Smart/Intelligent Textiles |

$22.08 Billion |

$29.23 Billion |

Integrated Biometric Sensors |

|

Brut/Raw Denim |

$4.80 Billion |

$5.40 Billion |

Zero-Wash Longevity Models |

|

Technical Embroidery |

$1.59 Billion |

$1.69 Billion |

Conductive Thread Connectivity |

|

Bio-Based Textiles |

$54.21 Billion |

$58.80 Billion |

Regenerated Agricultural Waste |

Regional Trajectories: The race for material superiority

As the global landscape shifts, 2026 is witnessing a clear division of labor among the world’s textile powerhouses, each leveraging specific technological or regulatory advantages to capture market share.

China: The infrastructure of Circularity

In 2026, China has successfully transitioned from a volume-based manufacturer to the global hub for advanced textile recycling. The market for recycled materials in China is projected to lead the Asia-Pacific region, with a 4.9% CAGR driving revenues toward $416 million by the end of the year. Massive joint ventures are now unlocking up to 100,000 tonnes of textile-to-textile recycled PET spinning capacity annually. By integrating IoT and Bluetooth Low Energy (BLE) into high-output performance lines, Chinese mills are securing their position as the primary suppliers for the "Intelligent Textile" boom, providing the scale necessary to move smart fabrics into the mid-market price bracket.

European Union: The regulatory standard-setter

The EU continues to act as the primary catalyst for the "Brut" movement through aggressive legislative frameworks. With the July 2026 ban on the destruction of unsold apparel, European buyers are prioritizing "Demand-Responsive" fabrics; materials that allow for late-stage digital printing or modification to prevent overproduction. The focus here is on the "Quality Premium," where the environmental footprint of every square meter is tracked. This has created a massive market for "Digital Product Passport" (DPP) ready textiles, where transparency is treated as a high-value product feature.

India & Vietnam: The efficiency powerhouses

India and Vietnam have moved aggressively into high-value Original Design Manufacturing (ODM). Vietnam’s textile exports are on track to reach $50 billion in 2026, fueled by a "dual transformation" of digitalization and greening. Vietnamese factories are increasingly utilizing AI-based vision systems for defect detection and automated packaging to offset rising labor costs. In India, a government-backed $1.6 billion investment in technical textiles has resulted in over 56% of new industry entrants focusing on "Clothtech" and "Protech" segments. By blending "Brut" textures with recycled stretch fibers, Indian manufacturers are capturing a growing share of the premium sustainable denim market.

North America: The innovation hub

North America remains the global leader in smart clothing demand, holding a 48.4% share of the wearable textile market. In 2026, the US consumer will be the primary driver for "Function + Fashion," with a specific focus on medical and fitness integration. This demand has pushed US-based manufacturers to focus on "Very Smart" textiles,fabrics that can recognize and adapt to environmental changes, transforming the garment from a passive product into an active participant in the user's healthcare and wellness ecosystem.

Regional economic & innovation outlook (2025-2026)

|

Region |

2025 Output (Est) |

2026 Export Forecast |

Strategic Competitive Advantage |

|

China |

$880 Billion |

$925 Billion |

Circular Economy Scale & IoT Integration |

|

European Union |

€162 Billion |

€170 Billion |

Regulatory Compliance & High-End Design |

|

India |

$152.4 Billion |

$164.8 Billion |

Technical Textiles & Organic Cotton Lead |

|

Vietnam |

$47.5 Billion |

$50.0 Billion |

Smart Factory Automation & ESG Hub |

|

North America |

$196.4 Billion |

$204.5 Billion |

Smart Textile Demand (48% Global Share) |

The C-Suite Outlook: Strategic resilience and the "Service" of surface

For the leadership tiers of 2026, the focus has shifted from managing commodities to managing sophisticated software delivery systems. The "Orchestrator CEO" of 2026 recognizes that the fabric surface is no longer a passive substrate but a functional service. Market winners are those who have abandoned the binary choice between sustainability and performance, instead using technology as the bridge to make circularity profitable. Leadership is now centered on data-first sourcing, where a roll of fabric is evaluated not just on its weight or hand-feel, but on its digital twin and its capacity for lifecycle tracking.

Editor’s Conclusion: The era of the intelligent loom

As we conclude our look at the transition from 2025 to 2026, the overarching theme is the end of the "middle ground." The textile industry has reached a point where value is created at the extremes—either through the raw, unrefined honesty of "Brut" materials or the hyper-engineered capabilities of smart fabrics. The loom of 2026 is digital, the thread is circular, and the business model is defined by transparency. In this new era, the most successful B2B partnerships will be those that can deliver a narrative as authentically raw as it is technologically advanced. The fabrics of 2026 are no longer just clothing; they are the most sophisticated interfaces on the planet.

French luxury titan LVMH has finalized its 100 per cent acquisition of Les Editions Croque Futur, absorbing influential titles Challenges, Sciences & Avenir, and La Recherche into its UFIPAR investment vehicle. This maneuver transitions LVMH from a minority stakeholder (previously holding 40 per cent) to the sole proprietor, buying out founder Claude Perdriel. The move is viewed by retail analysts as a strategic effort to control high-value business and scientific discourse, paralleling LVMH’s existing ownership of Les Echos and Le Parisien. Market experts suggest this ‘information luxury’ model allows the group to align its brand prestige with intellectual authority in an increasingly volatile digital economy.

Digital transformation and commercial resilience

The acquisition comes at a pivotal moment as the French advertising market is projected to reach €28.5 billion by late 2025. LVMH plans to accelerate the digital evolution of these mastheads to ensure long-term viability amidst shifting readership habits. By appointing Maurice Szafran as President, the group is signaling a commitment to editorial continuity while leveraging its deep capital reserves to modernize scientific and economic reporting. Retail insiders note,as LVMH reports steady revenue growth - surpassing €58 billion in the first nine months of 2025 - the group is utilizing its robust balance sheet to insulate these media assets from the wider industry’s ‘whipsaw’ market conditions.

Luxury ecosystem expansion and sector impact

This full integration reinforces a broader trend of ‘brand ecosystem’ building, where luxury conglomerates own the channels that define cultural and economic status. The addition of Challenges - famous for its annual ranking of French fortunes - places LVMH in a unique position of influence over the very metrics that track its industry’s success. While the editorial staff has emphasized the need for independence, LVMH’s track record with Paris Match and Radio Classique suggests a model where financial stability is traded for strategic alignment with the group’s ‘Art of Crafting Dreams’ philosophy.

The world’s leading high-quality products group, LVMH operates across five sectors, including Fashion, Wines & Spirits, and Selective Retailing. Managed via UFIPAR, its media arm focuses on prestigious French mastheads. With 2024 revenues of €84.7 billion and a net profit of €12.6 billion, the group is aggressively expanding its cultural influence to supplement its core luxury industrial activities globally.

Wolverine World Wide (WWW) is successfully navigating a complex 2026 fiscal landscape by concentrating its marketing capital into elite urban hubs, a move that has effectively insulated its flagship brands from broader sector volatility. While the group anticipates an incremental $55 million unmitigated tariff impact this year, the ‘Active Group’ - comprising Saucony and Merrell - continues to serve as a high-margin firewall. In particular, Saucony has maintained an aggressive growth trajectory, with recent data showing a 27 per cent Y-o-Y revenue growth. This momentum is anchored by the brand’s ‘Key City’ initiative, which prioritizes hyper-localized retail experiences in Tokyo, London, and Paris over traditional mass-market distribution.

Industrial innovation and APAC acceleration

Beyond performance running, the company is capturing a larger share of the modern outdoor lifestyle market through Merrell’s strategic expansion. No longer confined to technical hiking, Merrell is evolving into a versatile lifestyle brand, a shift that contributed to double-digit gains across EMEA markets. In the Asia-Pacific region, WWW is utilizing local partnerships to scale its footprint in China, targeting discerning consumers in higher-tier cities. Management expects APAC to remain the fastest-growing territory for Saucony through late 2026. This regional strength is boosted by the group’s ‘Strategic Innovation Hub,’ which integrates AI-driven market analysis and sustainable material science—factors that 47 per cent of outdoor consumers now cite as a primary purchase driver.

Operational discipline amidst market bifurcation

As the footwear industry experiences a distinct ‘K-shaped’ recovery, WWW has maintained price integrity by reducing promotional activity and optimizing its inventory mix. This financial discipline resulted in a record gross margin of 47.5 per cent in the most recent quarter. While the Work Group segment has faced headwinds, the appointment of new leadership and the launch of the ‘Infinity System’ platform for industrial boots aim to stabilize the category. By focusing on disruptive innovation rather than volume-driven sales, WWW remains positioned to exceed its projected $1.87 billion revenue guidance, demonstrating resilience in a competitive landscape dominated by high-income consumer demand for athleisure and performance footwear.

Headquartered in Rockford, Michigan, Wolverine World Wide manages a diverse portfolio including Merrell, Saucony, and Sweaty Betty across 170 countries. The company focuses on the Active, Work, and Lifestyle categories, projecting $1.87 billion in 2025 revenue.

Everlert, Inc has successfully closed a strategic reverse merger with Zanieri SpA, a vertically integrated Italian luxury knitwear powerhouse. Under the finalized agreement, Zanieri assumes controlling interest in the public entity, transitioning the Perugia-based manufacturer into a US-listed platform. Historically, Zanieri has operated as a critical backbone for the global luxury sector, with over 70 per cent of its revenue derived from ‘white label’ manufacturing for leading international fashion houses. However, the new corporate structure is designed to invert this model, prioritizing the ‘Zanieri’ brand to become the primary revenue driver by 2026. Management intends to leverage its status as a top producer of premium, traceable-origin cashmere to capture a significant share of the premium menswear segment, which is projected to grow as consumers shift toward investment-grade apparel.

Digital bespoke technology and American expansion

A core component of Zanieri’s scalability is its proprietary remote tailoring platform, which allows the company to deliver customized, made-to-measure garments to global clients without the need for traditional physical fittings. This technology facilitates a high-margin ‘bespoke-at-scale’ model, which will be central to the brand's aggressive entry into the United States. Following FY2025 where 95 per cent of gross sales originated in Europe, the company has identified New York as its primary commercial gateway. Plans are underway to launch a flagship mono-brand store in Manhattan alongside a proprietary direct-to-consumer (DTC) e-commerce site. This ‘Mediterranean heritage meets modern tech’ strategy aims to fill the market void between mass-market fashion and inaccessible haute couture.

Sustainable infrastructure and global market resilience

Operating from Umbria, the global ‘cashmere capital,’ Zanieri controls every stage of production - from yarn selection to finishing. This vertical integration provides a rare level of transparency and sustainability in an industry facing increasing regulatory pressure regarding supply chain ethics. While current operations focus on knitwear and home textiles, the long-term roadmap includes diversification into yachting, golf, and equestrian lifestyle categories, with a future extension into womenswear. By utilizing its robust manufacturing infrastructure and public company status, Zanieri is positioned to insulate itself from broader market volatility while executing a disciplined expansion into high-growth hospitality and B2B luxury partnerships.

Based in Perugia, Italy, Zanieri is a premier vertically integrated producer of sustainable cashmere and luxury knitwear. Controlling the entire lifecycle from dye science to assembly, the company serves as a major manufacturer for global brands while rapidly scaling its own premium label through proprietary remote-tailoring technology and a planned US retail expansion.

To help you optimize the Zanieri and Everlert merger story for your audience, here are the strategic focus keywords and a selection of question-driven meta descriptions.