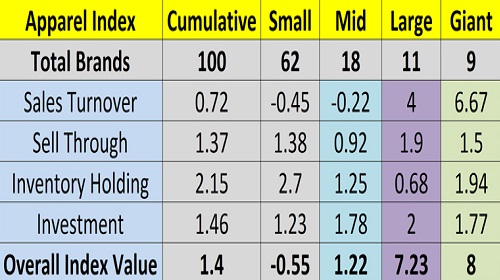

"CMAI’s Apparel Index for Q3 Oct-Dec FY 2016-17 shows this quarter had the lowest growth so far with overall Index Value at 1.4 points compared to previous quarter (July-Sept FY 2016-17) where overall Index Value was 4.64 points. The dismal growth last quarter is fallout of ‘Demonetisation’ that impacted all segments and sectors of Indian economy including the apparel industry. Within apparel industry, the impact has been felt across the board. However, big brands seem to have adapted and managed growth. While Large Brands (turnover of Rs 100 to Rs 300 crores), were at 7.23 and Giant Brands (turnover of R 300 crores and more) scored 8 points respectively."

CMAI’s Apparel Index for Q3 Oct-Dec FY 2016-17 shows this quarter had the lowest growth so far with overall Index Value at 1.4 points compared to previous quarter (July-Sept FY 2016-17) where overall Index Value was 4.64 points. The dismal growth last quarter is fallout of ‘Demonetisation’ that impacted all segments and sectors of Indian economy including the apparel industry. Within apparel industry, the impact has been felt across the board. However, big brands seem to have adapted and managed growth. While Large Brands (turnover of Rs 100 to Rs 300 crores), were at 7.23 and Giant Brands (turnover of R 300 crores and more) scored 8 points respectively. Small brands (turnover of Rs 10-25 crores) however, have been hit badly recording negative growth at -0.55 points, while mid brands (turnover of Rs 25 to 100 crores) managed to grow a meager 1.22 points.

Big brands, maintained growth with fast clearance off goods and discounts that increased Sales Turnover to 4 and 6.67 points and reduced inventory holding increase to just 0.68 and 1.77 points respectively. Comparatively, Small and Mid brands lost Sales Turnover this quarter by 0.45 and 0.22 points and Inventory Holding increased for Small Brands at 2.70 and Mid Brands at 1.25 points. This had a cumulative impact on Sales Turnover and Inventory Holding of Overall Index Value as Small brands and Mid brands outnumber Large and Giant Brands greatly.

Large and Giant brands continue lead

Q3 Apparel Index clearly indicates that large and giant brands have outdone mid and small brands. Small and mid brands lost sales turnover, and one of the main reasons could be demonetization and its impact on overall retail sales. Smaller retailers and brands associated with them had much larger transactions based on cash instead of credit cards or other digital modes. Drop in sales impacted stocks clearance and hence, increased Inventory Holding affecting doubly the Index value of both (small and mid brands). Large brands and giant brands on the other hand, connected with organized retail through MBOs, EBOs and Large Format Stores took the deep discounting route thereby stimulating sales to clear off inventory at store and company level this is clearly reflected in increased Sales Turnover and restricted Inventory Holding in effect pushing up their Index at 7.23 and 8 points.

Since small and mid brands are more dependent on trade and have less control on retail, they couldn’t push sales, while large and giant brands could stimulate sales turnover thereby restricting Inventory Holding. As Vineet Gautam, Country Head, Bestseller India explains, “We have seen more than 50 per cent surge in sales for ONLY compared to last year. We had planned and added 40 new doors to the brand, which automatically implied an increase in inventory holding. Also, the key to managing increased inventory holding is increasing sell out. For ONLY, we successfully managed to increase sell out.” Arguing on similar lines Anant Daga, VP, ‘W’ and Aurelia, says, “Sales growth surge is backed by high double digit SSSG and aggressive expansion. Inventory reduction is a result of better than expected sales against planned buys.” Explaining the plight of winter wear makers and retailers which was impacted the most due to demonetization Vinod Kumar Gupta, MD, Dollar Industries, says, “Some of our products like thermals are seasonal in nature and production had been done in the month of July and August, to be sold up in winter months. But with demonetization, the entire industry witnessed a drastic fall in the last quarter. Naturally our inventory increased by a huge margin. But with summer approaching and the new financial year, we are hoping all summer products are sold and closing stock goes down.”

Classis Polo attributes increased Sales Turnover and better Sell Through, to a better designed product that catches consumers’ fancy. As Usha Periasamy, VP - Operations & Brand, Classis Polo opines, “Fine research in understanding the design needs of the target group and market thereby upgrading creativity to meet expectations precisely. Earlier, Classic Polo range had striper dominated tee's and basic collections but now non striper fashion category has taken over which is reaping results. We have identified the most liked categories in shirts and trousers viz., printed shirts and Lycra bottoms are order of the day.” In fact, brands getting closer to customer expectations and is the real reason behind turnover and sales push. This effect will be more evidently in the next fiscal. In fact around 41 per cent brands feel the outlook for next quarter is ‘Good’, another 10 per cent say the outlook is ‘Excellent’. Nearly 42 per cent foresee an average outlook and 7 per cent (previous quarter also 2) feel it will be ‘Below Average’. Next quarter being the last quarter of the year, brands assume demonetization impact though phasing out will still be there as consumers will take time to return to stories.

About CMAl's Apparel Index

CMAl's Apparel Index, conducted by DFU Publications aims to set a benchmark for the entire domestic apparel industry and helps brands in taking informed business decisions. For investors, industry players, stakeholders and policymakers the index is a useful tool offering concrete and credible information, and is an excellent source for assessing the performance of the industry. The Index is analysed on assessing the performance on four parameters: Sales Turnover, Sell Through (percentage of fresh stocks sold), number of days of Inventory Holding and Investments (signifying future confidence) in brand development and brand building. The Apparel Index research is conducted by DFU Publications.